Many individuals believe that achieving financial freedom is reserved for those who hit the jackpot, receive massive inheritance, or possess advanced degrees in economics. However, true wealth is rarely the result of a single monumental event. Instead, it is the cumulative effect of small, consistent actions performed with intention every single day. By dedicating just ten minutes of your morning to a structured financial routine, you can gain total control over your fiscal future and build a foundation for long-term prosperity.

The Philosophy of Micro-Financial Management

Financial stress often stems from a lack of clarity. When we allow our money to drift without oversight, we lose the ability to make intentional choices. The secret to wealth building isn’t found in complex algorithms or intricate investment models; it is found in the consistency of your character. By adopting a ‘micro-habit’ approach to your personal finances, you replace fear and ambiguity with actionable data and confidence.

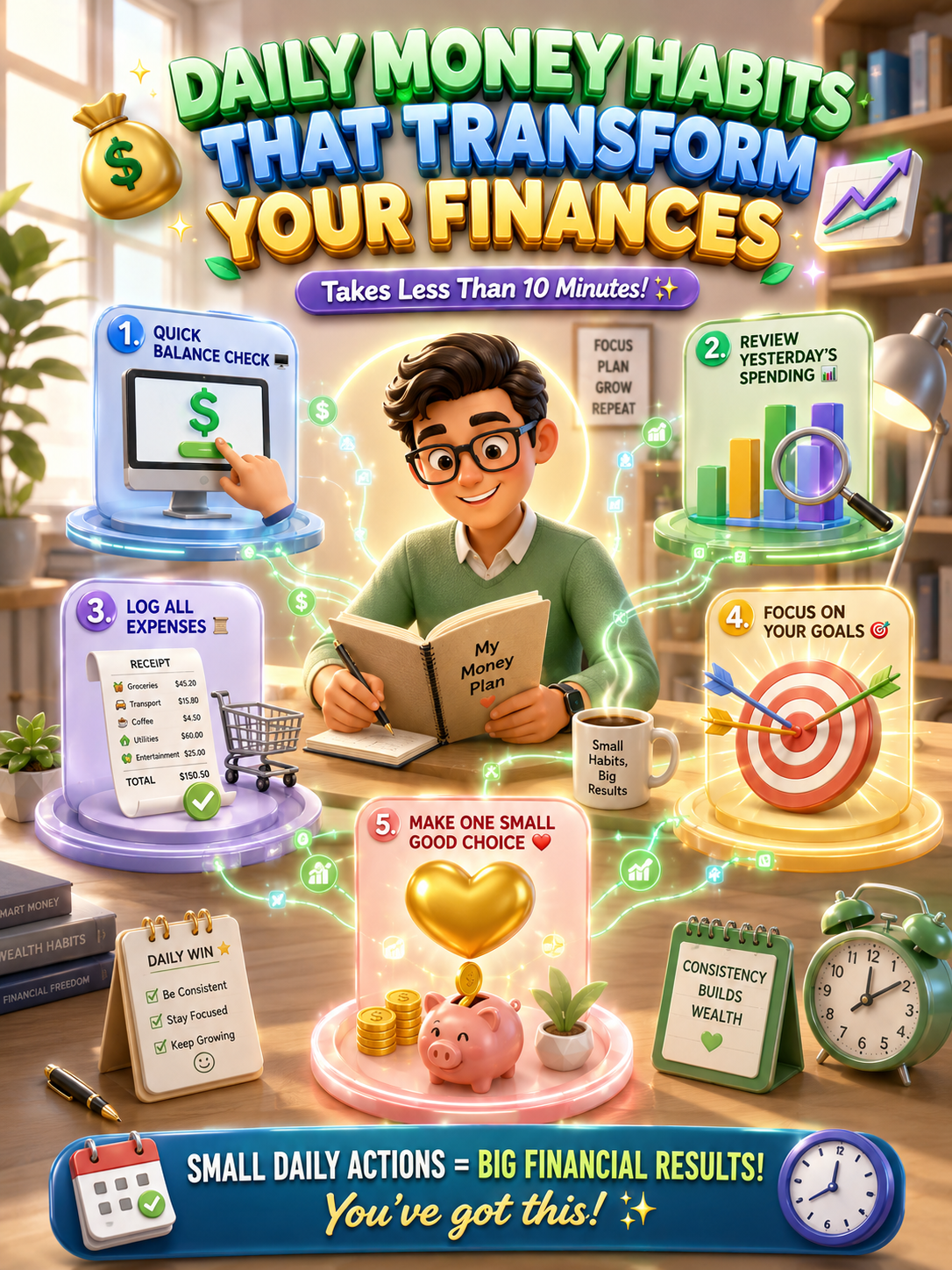

1. The Power of Awareness: Daily Account Surveillance

The most common barrier to financial growth is ‘ostrich syndrome’—the tendency to bury one’s head in the sand to avoid looking at bank statements or credit card balances. This behavior typically stems from a fear of what the numbers might reveal. Yet, you cannot improve what you refuse to measure.

The Morning Two-Minute Check: Spend two minutes every morning reviewing your primary bank and credit card accounts. This is not about being paranoid; it is about establishing a rhythm of awareness. By doing this regularly, you gain three distinct advantages:

- Fraud Detection: Identifying an unauthorized charge immediately allows you to dispute it before it becomes a major problem.

- Situational Awareness: You will always know your exact ‘starting point’ for the day, which prevents accidental overspending.

- Psychological Tranquility: There is a profound peace of mind that comes from knowing exactly where you stand, effectively eliminating the background anxiety of ‘financial mystery.’

2. Reflective Analysis: Evaluating Yesterday’s Decisions

Once you are aware of your current standing, you must look backward briefly. Reviewing the previous day’s expenditures is a powerful method for identifying ‘lifestyle creep.’ Lifestyle creep refers to the gradual increase in spending as our income grows, often masked by small, seemingly insignificant daily purchases.

Spotting the Trends: When you review your yesterday’s spending, look for patterns. Did you buy a coffee that you could have made at home? Did an automated subscription renew that you no longer utilize? By catching these micro-leaks in your budget, you plug the holes in your financial bucket before they drain your savings.

3. The Discipline of Real-Time Tracking

Memory is a poor substitute for data. We often believe we know where our money is going, but the reality is frequently different from our perceptions. To genuinely master your wealth, you must document every expense as it happens. Using a high-quality budgeting app or a simple digital ledger creates ‘psychological friction.’ This friction acts as a barrier to impulsive, mindless spending, forcing you to think twice before tapping your card.

Categorization as a Tool for Growth: Effective tracking goes beyond logging numbers; it is about categorizing your life. When you see exactly how much of your hard-earned income is directed toward dining out versus essential investments, the need to adjust your behavior becomes obvious. Accountability is the bridge between wanting wealth and actually achieving it.

4. Keeping Your Vision in Sharp Focus

Routine tasks can become tedious if you lose sight of the objective. Every day, take a brief moment to visualize your financial goals. Whether you are aiming to eliminate high-interest debt, build an emergency fund, or save for a major purchase, your goals must serve as the compass for your daily choices.

Goal-Based Spending: When you are tempted to purchase an unnecessary item, frame the decision against your larger vision. Ask yourself: ‘Does this specific expenditure move me closer to my goal of financial independence, or does it take me further away?’ This simple mental check is the primary differentiator between those who struggle with money and those who grow it.

5. The Closing Ritual: Choosing One Positive Action

Finish your daily money routine with a proactive step. By focusing on a ‘positive action’ rather than ‘restriction,’ you build your financial willpower. You don’t need to perform a miracle; you simply need to make one smart choice that benefits your future self.

Examples of Smart Daily Moves:

- Packing a lunch to avoid delivery fees.

- Transferring a small, manageable amount into a high-yield savings account.

- Researching more competitive rates for your monthly utility bills.

- Opting for a generic brand to maximize value during a grocery run.

These seemingly small actions build ‘wealth muscle.’ Over time, these habits become second nature, and the discipline required to maintain them diminishes, while the rewards continue to multiply.

Addressing Common Financial Hurdles (FAQ)

How long does this entire routine take?

An effective daily money routine is designed for speed and consistency, taking ten minutes or less to complete.

Why should I track expenses if I use a budget?

Budgets are plans; tracking is the reality check. Tracking ensures that your actual behavior remains aligned with your budgetary intentions.

Is technology necessary for this process?

While digital apps offer convenience, the key is the method, not the tool. Whether you use a complex spreadsheet or a notebook, the most important element is that you consistently record and review your financial data.

What if I miss a day of tracking?

Financial management is a marathon, not a sprint. If you miss a day, simply pick it up the next morning. The goal is long-term consistency, not temporary perfection.

Does this really lead to ‘wealth’?

Wealth is built through the compound interest of both money and habits. By refining your spending and saving choices daily, you create a financial momentum that compounds over years and decades.

Conclusion: Your Future Self Will Thank You

The journey to financial prosperity is paved with the small, quiet choices you make when nobody is watching. By implementing these five essential habits—maintaining awareness, reviewing previous spending, tracking expenses in real-time, aligning with your goals, and committing to one positive financial choice daily—you are constructing a robust, sustainable financial future. Remember, you do not need to be perfect to succeed; you simply need to be present and engaged. Start your 10-minute ritual today, and begin the transformation of your personal finances.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Always consult with a professional financial advisor regarding significant money decisions.