10 Indicators Your Financial Management Requires Urgent Attention (And How to Course Correct)

Mastering personal finance is a cornerstone life skill, yet countless individuals grapple with financial behaviors that insidiously undermine their future well-being. Ineffective money management often doesn’t manifest dramatically at first. Instead, it can creep in through seemingly minor daily habits that gradually lead to mounting debt, persistent stress, and overall financial instability. If you frequently feel overwhelmed by your financial situation, it’s probable that warning signs are lurking within your everyday routines. Identifying these signals early is crucial for averting significant financial calamities and building a more resilient financial framework. Here are the ten most telling signs that your approach to managing money needs a serious re-evaluation—and practical steps you can take to enhance your financial health.

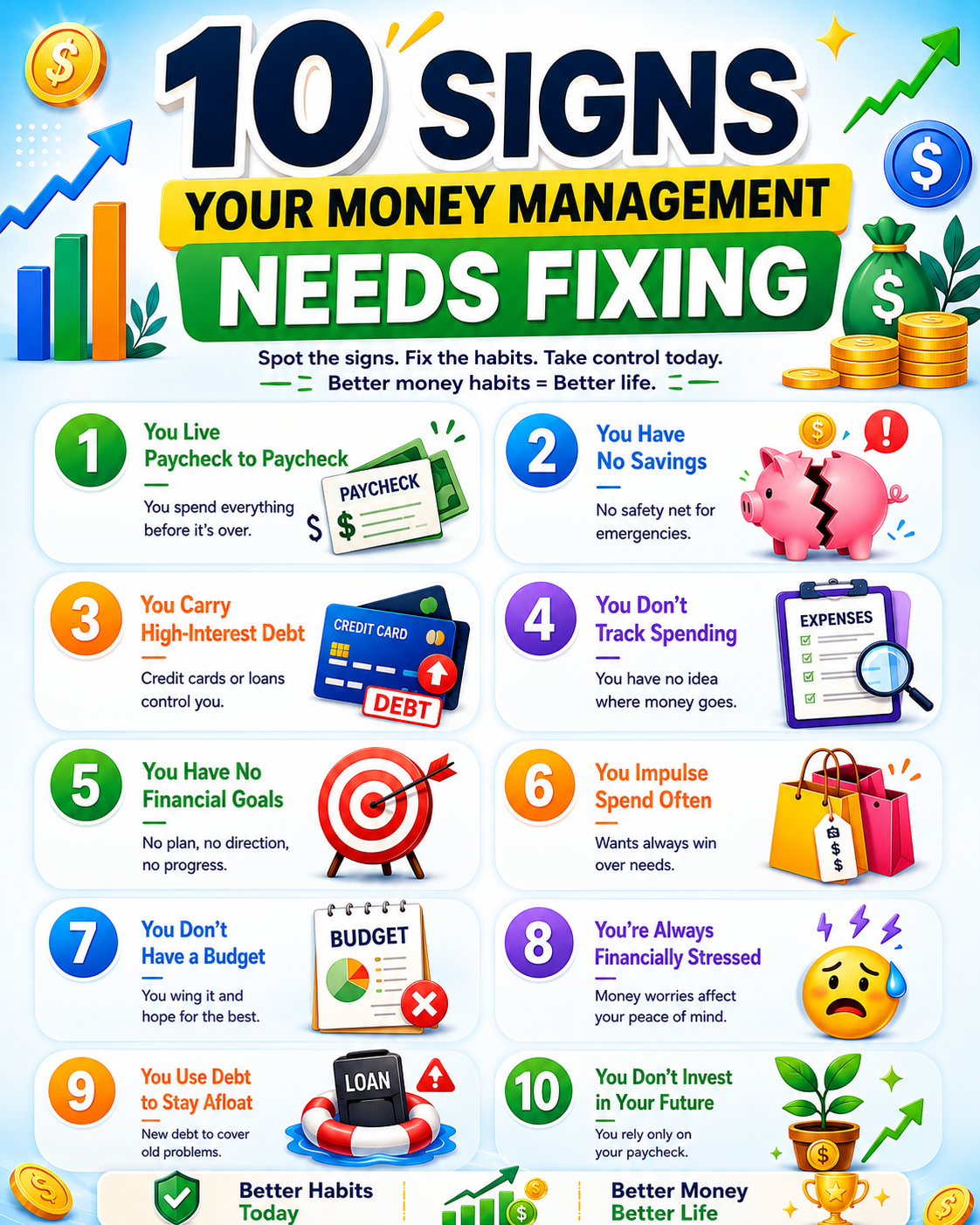

1. Living on the Edge: The Paycheck-to-Paycheck Cycle 💸

One of the most unambiguous indicators of underdeveloped financial management is the complete reliance on each incoming paycheck solely for subsistence. When all your income is depleted before the subsequent payday arrives, the capacity to save, invest, or adequately prepare for unforeseen circumstances becomes severely compromised. Even a minor, unexpected expense can trigger substantial financial anxiety.

Common Triggers for This Cycle:

- Excessive spending on lifestyle enhancements and non-essentials.

- High monthly debt repayment obligations.

- Absence of a structured budget.

- Escalating cost of living.

- Lack of consistent saving discipline.

Strategies for Breaking Free:

- Meticulously track every single outgoing expense each month.

- Prune or eliminate unnecessary subscription services.

- Initiate the establishment of a foundational emergency fund.

- Prioritize spending on essential needs above all else.

- Develop and adhere to a practical and realistic monthly budget.

The perpetual state of living paycheck to paycheck often ensnares individuals in a relentless loop of financial worry. The key to escaping this predicament lies in achieving clarity regarding precisely where your money is being allocated. 🎯

2. The Void of Savings: No Financial Safety Net 🐷

A dedicated savings account serves as a vital pillar of financial security and promotes a sense of calm. In its absence, every unexpected event escalates into a full-blown financial crisis. A deficit in savings frequently translates to:

- Zero protection against emergencies.

- Increased dependence on borrowed funds.

- Pervasive financial pressure.

- Significant obstacles in achieving personal financial objectives.

The Indispensable Role of Emergency Funds:

Unforeseen circumstances, such as substantial medical bills, sudden job loss, critical car repairs, or urgent travel necessities, can arise without warning. An emergency fund is instrumental in minimizing reliance on high-interest loans and credit cards during these trying times. 🏥🚗

Smart Approaches to Building Savings:

- Automate regular transfers of funds into your savings account each month.

- Begin with small, manageable amounts and maintain consistency.

- Opt for high-yield savings accounts to maximize returns.

- Allocate a predetermined percentage of every paycheck directly to savings.

- Consciously reduce or eliminate impulse purchasing behaviors.

Financial advisors generally recommend accumulating savings equivalent to three to six months’ worth of essential living expenses. 💰💼

3. The Debt Avalanche: Escalating Credit Card Balances 💳

Credit cards can be powerful financial instruments when utilized with prudence. However, a perpetually increasing balance coupled with high interest rates is a profound warning sign of financial imbalance.

Ominous Indicators of Debt Issues:

- Consistently making only the minimum required payments.

- Using one credit card to settle balances on another.

- Frequently reaching or exceeding credit card limits.

- Depending on credit cards to cover fundamental living expenses.

The accumulation of interest charges can rapidly transform modest purchases into burdensome, long-term financial obligations. 📈

Effective Strategies for Debt Reduction:

- Prioritize aggressively paying down the highest-interest debts first.

- Cease all non-essential credit card usage immediately.

- Explore debt consolidation options if feasible and beneficial.

- Commit to making monthly payments that significantly exceed the minimum.

- Avoid making spending decisions driven by emotional impulses.

Successfully reducing debt not only enhances financial agility but also substantially boosts long-term wealth-building potential. 💪

4. The Blind Spot: Neglecting Expense Tracking 📋

A significant number of individuals underestimate their monthly expenditures simply because they fail to diligently monitor their financial outlays. Without a systematic approach to tracking expenses:

- Overspending becomes an unacknowledged norm.

- Financial aspirations lose clarity and focus.

- Savings dwindle at an alarming rate.

- Unseen budget leaks persist unnoticed.

Commonly Overlooked Spending Categories:

- Food delivery services and takeout.

- Subscriptions for streaming platforms and apps.

- Impulsive online shopping sprees.

- Numerous small, seemingly insignificant daily purchases.

- Unplanned, spontaneous buys.

Straightforward Methods for Monitoring Spending:

- Leverage dedicated budgeting applications on your smartphone.

- Review your bank and credit card statements weekly.

- Consistently categorize each expenditure.

- Establish firm monthly spending limits for various categories.

- Pay close attention to discretionary and non-essential purchases.

The act of tracking your money cultivates a profound awareness—and this enhanced awareness is the catalyst for making more astute financial decisions. 🧠💡

5. Drifting Without Direction: The Absence of Financial Goals 🎯

Money that lacks a clear purpose or objective tends to dissipate rapidly. Establishing concrete financial goals is essential for fostering discipline, providing direction, and ensuring long-term stability.

Examples of Salutary Financial Objectives:

- Amassing a substantial emergency fund.

- Saving for the significant purchase of a home.

- Achieving complete freedom from debt.

- Securing adequate funds for retirement.

- Generating passive income streams for financial flexibility.

The Crucial Importance of Setting Goals:

Financial objectives serve as a vital compass, guiding spending decisions and motivating consistent saving behaviors. They transform abstract financial aspirations into tangible targets. 🧭

Effective Goal-Setting Principles:

- Ensure all goals are specific and measurable.

- Set realistic and achievable deadlines for each goal.

- Deconstruct large, ambitious goals into smaller, manageable milestones.

- Regularly review your progress toward achieving each goal.

- Be prepared to adjust your goals as circumstances evolve.

Well-defined objectives shift money management from a reactive necessity to a proactive, intentional planning process. ✨

6. The Urge to Splurge: Frequent Impulsive Purchases 🛍️

Impulse buying represents one of the most rapid routes to derailing a carefully constructed budget. Contemporary marketing strategies, the pervasive influence of social media, and the convenience of online shopping platforms frequently encourage emotional purchases that offer only fleeting moments of satisfaction.

Indicators of Problematic Impulse Spending:

- Acquiring items that are rarely or never used.

- Shopping as a coping mechanism when feeling stressed, bored, or sad.

- Engaging in frequent, unplanned online purchases.

- Overspending significantly during sales events or promotions.

- Experiencing regret or buyer’s remorse shortly after a purchase.

Techniques to Curb Impulse Spending:

- Implement a 24-hour waiting period before finalizing non-essential purchases.

- Always shop with a predefined list of necessary items.

- Consciously avoid shopping when experiencing strong emotions.

- Minimize exposure to social media platforms that promote shopping.

- Set strict spending limits for discretionary categories.

Cultivating mindful spending habits not only enhances your financial health but also strengthens your emotional resilience and self-control.🧘♀️

7. The Budget Black Hole: Lack of a Financial Plan 📉

A budget is not intended to be a tool of severe restriction; rather, it is designed to empower you to control your money, rather than allowing your money to control you. In the absence of a budget:

- Spending patterns become erratic and unpredictable.

- Savings efforts are inconsistent and often fall short.

- Debt accumulation occurs more readily and can spiral out of control.

- The achievement of financial milestones is significantly delayed.

Components of a Robust Budget:

- Essential fixed expenses (rent/mortgage, utilities).

- Planned savings contributions and allocations.

- Scheduled debt repayment amounts.

- Provisions for an emergency fund.

- Allocated funds for personal discretionary spending categories.

Popular Budgeting Methodologies:

- The 50/30/20 Rule: A straightforward guideline allocating 50% of income to needs, 30% to wants, and 20% to savings and debt repayment. 📊

- Zero-Based Budgeting: A meticulous approach where every single dollar of income is assigned a specific purpose or allocation before any spending commences. 💸

The implementation of a budget provides essential structure, fosters accountability, and cultivates a profound sense of financial confidence. ✅

8. The Constant Worry: Pervasive Money-Related Stress 😟

Financial stress can have a detrimental impact on mental well-being, interpersonal relationships, sleep quality, and overall life satisfaction. If concerns about money frequently occupy your thoughts and cause significant distress, it is a strong indication of underlying issues in your financial management practices.

Common Contributors to Financial Anxiety:

- Ever-increasing levels of debt.

- The absence of a sufficient savings buffer.

- Unwise or excessive spending habits.

- Income streams that are unpredictable or unstable.

- A complete lack of a coherent financial plan.

Effective Strategies for Alleviating Financial Worry:

- Develop and commit to a realistic and actionable financial plan.

- Create and implement systematic debt repayment strategies.

- Conscientiously avoid unnecessary borrowing and incurring new debt.

- Invest in improving your financial literacy and knowledge.

- Focus on making consistent, incremental progress toward your goals.

Financial confidence flourishes when your approach to managing money becomes organized, intentional, and strategic. 🌟

9. The Cycle of Borrowing: Constantly Relying on Loans 🆘

The practice of regularly taking out loans or using credit to cover essential daily expenses is a serious and alarming financial red flag. Depending on borrowed funds for necessities often signifies:

- Instability in your primary income sources.

- A pattern of overspending beyond your means.

- Fundamental flaws in your budgeting approach.

- A critical absence of emergency savings.

The Significant Risks Associated with Perpetual Borrowing:

- Accumulation of substantial high-interest payments over time.

- Entrenchment in a cycle of debt dependency.

- Potential damage to your credit score and financial reputation.

- Increased overall financial instability and vulnerability.

More Sustainable Alternatives to Borrowing:

- Implement drastic reductions in non-essential expenditures.

- Actively explore and develop multiple income streams.

- Institute and strictly adhere to extremely disciplined budgets.

- Focus on building an emergency savings fund gradually but consistently.

Breaking free from the cycle of constant borrowing is absolutely paramount for achieving genuine financial independence and autonomy. 🗝️

10. Future Blindness: Forgetting to Invest for Tomorrow 🌱

While diligently saving money is a crucial step, it is often insufficient on its own for building significant long-term wealth. Investing your money wisely allows it to grow exponentially over time through the power of compound returns. Individuals who shy away from investing may struggle to:

- Effectively counteract the erosion of purchasing power caused by inflation.

- Accumulate the substantial capital required for a comfortable retirement.

- Establish meaningful passive income streams to supplement earnings.

- Attain true financial freedom and the ability to live life on your own terms.

Accessible Investment Avenues for Beginners:

- Index Funds: Low-cost funds that track a specific market index. 📈

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other securities. 📊

- Retirement Accounts (e.g., 401(k), IRA): Tax-advantaged accounts designed for long-term savings. 👴👵

- Dividend Stocks: Shares in companies that regularly distribute a portion of their profits to shareholders. 💵

- ETFs (Exchange-Traded Funds): Similar to mutual funds but trade on stock exchanges like individual stocks. 🚀

The Profound Importance of Investing:

Long-term investing is a powerful mechanism for wealth creation, capable of generating significant returns even with modest monthly contributions. The principle of starting early often holds more weight than the amount initially invested. ⏳💰

Revitalizing Your Financial Management: A Roadmap to Improvement 🔧

Transforming ingrained money management habits is a journey, not an overnight event. However, the consistent implementation of small, deliberate actions can precipitate profound financial metamorphosis over time. Cultivating these key financial habits is essential:

- ✅ Diligently track your spending on a regular basis.

- ✅ Adhere to a realistic and achievable budget.

- ✅ Actively build and maintain an emergency savings fund.

- ✅ Systematically reduce and eliminate unnecessary debt.

- ✅ Practice mindful and avoid emotional spending.

- ✅ Invest consistently for long-term growth.

- ✅ Clearly define and pursue your financial goals.

- ✅ Continuously enhance your financial knowledge and education.

Financial success is seldom solely about earning vast sums of money. It is predominantly forged through unwavering discipline, steadfast consistency, and the art of making intelligent, informed decisions. 💯

Concluding Thoughts: Embracing Financial Transformation 💡

The insidious effects of poor money management can subtly undermine financial stability for years before conspicuous problems emerge. The most encouraging news is that financial habits are inherently malleable and can always be improved through heightened awareness and decisive action. If you recognize several of these critical warning signs within your own financial landscape, view this not as a declaration of failure, but as a powerful opportunity to fundamentally reset and redirect your financial strategy. Embracing superior budgeting practices, cultivating smarter spending habits, committing to consistent saving, and engaging in strategic long-term investing can gradually transmute financial stress into unshakeable financial confidence. 🚀

💰 Small, positive adjustments made today have the potential to blossom into a significantly more secure and financially independent tomorrow.

Frequently Asked Questions (FAQ)

❓ What is the most significant indicator of poor money management?

A: Consistently living paycheck to paycheck and struggling to meet basic expenses are major signals of underdeveloped money management skills.

❓ Why is adhering to a budget so crucial?

A: Budgeting provides essential control over spending, facilitates increased savings, aids in debt reduction, and is fundamental to achieving your financial aspirations.

❓ What is the recommended amount for an emergency fund?

A: Many financial experts advocate for accumulating an emergency fund that covers three to six months of essential living expenses.

❓ How can one effectively control impulse spending?

A: Strategies such as creating shopping lists, implementing a waiting period before purchases, and setting clear spending limits can significantly curb impulsive buying behavior.

❓ What is the purpose of investing?

A: Investing is vital for enabling your money to grow over time, outpacing inflation, and building substantial long-term wealth.

❓ What are the common causes of financial stress?

A: Mounting debt, insufficient savings, excessive spending, and a lack of financial planning are frequent culprits behind financial stress.

❓ What are the initial steps to begin saving money?

A: Committing to small, automated savings contributions and actively reducing non-essential expenses are effective starting points for building savings.

❓ Could you explain the 50/30/20 budgeting rule?

A: The 50/30/20 rule is a budgeting framework that suggests allocating 50% of income to essential needs, 30% to discretionary wants, and 20% towards savings and debt repayment.

❓ What makes tracking expenses so important?

A: Tracking expenses provides crucial insights into spending patterns, helps identify areas of overspending, and enhances overall financial awareness.

❓ Is it possible to improve poor money habits?

A: Absolutely. Through consistent application of budgeting principles, diligent saving, strategic debt reduction, and proactive financial planning, money habits can be significantly improved over time.