Most people view financial success as a result of intense willpower or the ability to make high-stakes investment decisions. They spend their days meticulously tracking every penny or obsessing over the latest stock market trends. While those actions have their place, they often overlook the most powerful tool for long-term prosperity: the financial system.

The reality is that discipline is a limited resource. After a demanding day at the office, a long commute, or managing a household, your mental battery is likely depleted. Relying on sheer grit to make smart money decisions daily is a recipe for failure. Instead, those who achieve true financial security rely on automation and repeatable processes—or, in short, systems.

Why Willpower Isn’t Enough

Human psychology is fundamentally wired for immediate gratification. Our ancestors didn’t need to save for retirement; they needed to find food for the day. In the modern world, this translates into an instinct to spend when we see something shiny or appealing. When you try to override this impulse with nothing but “discipline,” you are fighting against your own biology.

By shifting your focus to building a system, you take the choice out of the equation. You are no longer asking yourself, “Should I save money today?” The decision was made months ago when you set up your automated transfers. You are essentially pre-programming your path to wealth, removing the friction that typically leads to spending leaks.

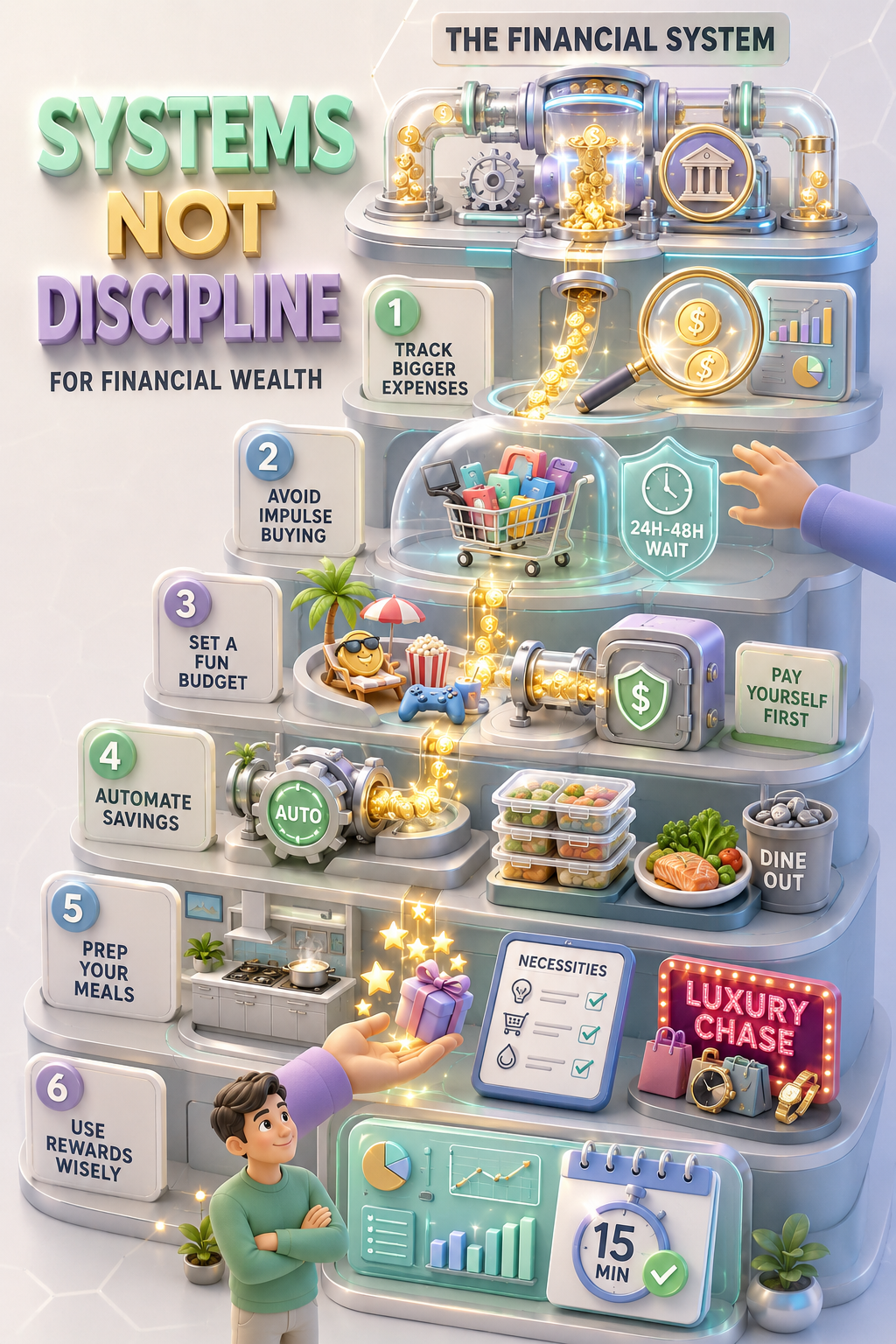

1. The Strategic Threshold: Tracking Significant Expenses

Many financial gurus advocate for extreme budget tracking, where you record the cost of every single cup of coffee. While this works for some, it causes burnout for most. The more efficient approach is to set a financial threshold.

Choose a baseline, such as $50 or $100. Any purchase that exceeds this amount must be logged and evaluated. By focusing on these larger outflows, you gain visibility into your biggest leaks—like high-interest subscriptions, luxury upgrades, or impulsive home purchases—without the exhaustion of tracking every trivial cent. When you see the big numbers in one place, you naturally become more cautious about how your money moves.

2. Mastering Impulse Control with the 24-48 Hour Rule

Impulse buying is the silent killer of wealth. We are often triggered by limited-time offers, social media influencers, or emotional spikes. To combat this, implement the 24-48 hour rule: if you want to buy something that isn’t a life-sustaining necessity, you must wait at least one or two days before finalizing the transaction.

In most instances, the initial dopamine rush fades, and you realize that the item isn’t actually necessary. This simple, system-based delay can save you thousands of dollars over the course of a year, effortlessly keeping cash in your bank account that otherwise would have vanished into non-essential goods.

3. Guilt-Free Spending with the “Fun Budget”

Rigid, restrictive budgets are destined for failure. Just like an overly strict diet, a budget that cuts out all pleasure will eventually lead to a “binge spending” episode. To create a system that lasts, you must account for your humanity.

Allocate a dedicated, fixed percentage or dollar amount to your “fun budget.” This is money that you are allowed to spend on anything you want without judgment or guilt. Knowing that you have this safety valve prevents you from feeling deprived, which in turn makes it significantly easier to stick to your long-term savings goals for the rest of your income.

4. The Golden Rule of Wealth: Pay Yourself First

If you leave your savings for the end of the month, you are essentially betting that there will be leftover money after your bills and impulses are satisfied. Experience shows us that there rarely is. To break this cycle, you must “pay yourself first.”

Automation is your best friend here. Set up an automatic transfer from your primary checking account to your savings or investment accounts for the same day your paycheck clears. By removing the money before you ever see it in your spending balance, you make saving a default setting rather than an optional task.

5. The Financial Multiplier: Meal Prepping

Dining out and ordering delivery are the most common invisible expenses that keep people from reaching their financial potential. Beyond being a health-focused lifestyle choice, meal prepping is a high-yield financial system.

By spending a few hours on a weekend to prepare your meals for the upcoming week, you eliminate the “convenience fee” of ordering out. When you calculate the cost of a restaurant meal versus home-prepared food, the difference over a month is staggering. This isn’t just about saving cash; it’s about creating a system that fuels your body and your bank account simultaneously.

6. Using Rewards Intentionally

Credit card rewards and cashback points are alluring, but they are designed to encourage spending. If you are charging extra purchases to your card just to hit a spending bonus, you have fallen into a trap. A 5% reward is meaningless if you are spending $100 on an unnecessary item just to get it.

Treat rewards as an incidental bonus for the spending you were already going to do. The system works when you align your card usage with your existing necessities. Never allow the allure of points to dictate your purchasing behavior.

7. The Weekly Command Center: The 15-Minute Review

You don’t need to spend hours buried in spreadsheets. However, you do need to have a pulse on your financial health. A weekly 15-minute review acts as your “command center.”

During this session, look at your bank balances, scan for errors or unauthorized charges, and verify that your recurring bills for the upcoming week are covered. This habit ensures that you catch small issues before they snowball into major financial crises. It keeps you proactive rather than reactive, giving you a sense of calm and control over your life.

Discipline vs. Systems: A New Philosophy

Discipline is a muscle that fatigues. Systems are machines that operate silently in the background. If you want to build lasting wealth, stop trying to be a hero every single day. Instead, be an architect.

By implementing these seven habits, you stop viewing yourself as someone who is “trying to save” and start embodying the identity of someone who “has a system.” This shift is the definitive moment where long-term financial success begins. When you stop relying on willpower and start relying on structure, you ensure that your progress is consistent, predictable, and—most importantly—sustainable.

Frequently Asked Questions

Why is a financial system better than using discipline?

Discipline is a finite resource that can fail when you are tired or stressed. A financial system automates your decisions, ensuring your money is managed correctly without requiring constant willpower.

What is the benefit of tracking only bigger expenses?

Tracking expenses over a set amount, such as $50 or $100, helps you identify significant financial leaks quickly without the burnout of logging every minor transaction.

How does the 24-48 hour rule stop impulse buying?

By waiting 24 to 48 hours before a purchase, the initial emotional spike and dopamine hit fade away, allowing you to decide if the item is a true need or just a temporary want.

What is a ‘fun budget’ and why is it necessary?

A fun budget is a set amount of money allocated for guilt-free spending. It is necessary to prevent feelings of deprivation, which often lead to major budget failures and binge spending.

How do I automate my savings effectively?

You can automate savings by setting up a recurring transfer from your checking account to your savings or investment account to trigger as soon as your paycheck arrives.

Can meal prepping actually save a significant amount of money?

Yes, meal prepping reduces the frequency of expensive dining out and delivery orders, often saving hundreds of dollars a month while improving your overall health.

What does it mean to ‘pay yourself first’?

Paying yourself first means prioritizing your savings and investments by moving that money out of your spending account before you pay bills or buy non-essentials.

How can I use credit card rewards without overspending?

Use rewards only for items you were already planning to purchase and avoid buying unnecessary things just to ‘chase’ more cashback or points.

What should I do during a 15-minute weekly financial review?

During a weekly review, check your bank balances, flag any errors or unwanted subscriptions, and look ahead at upcoming bills for the next week.

Why do most people fail to stick to a traditional budget?

Most traditional budgets are too restrictive and rely entirely on human discipline, which eventually runs out, leading to inconsistent habits.

How does automation remove financial temptation?

Automation moves money to its proper place before you even see it in your spending balance, making it much harder to spend your savings impulsively.

Is it better to track small expenses or large ones?

While all tracking is helpful, focusing on larger expenses provides a higher impact on your bottom line with much less effort and tracking fatigue.

What is the ‘cashback trap’?

The cashback trap is when a consumer spends more money than they intended just to earn a small percentage of rewards, resulting in a net financial loss.

Can a weekly financial review prevent major money problems?

Yes, a weekly review allows you to catch small errors, overspending, or missed payments before they turn into expensive fees or debt.

How does a financial system help build long-term wealth?

A system ensures that you are consistently saving and investing every single month regardless of your mood or motivation level, which maximizes compound interest over time.