📉 The Traditional Salary Trap: Why Liquid Income Limits Wealth Accumulation 💸

The conventional wisdom passed down through generations often emphasizes a linear path to financial success: excel in education, secure a high-profile corporate position, and earn a substantial annual salary. While achieving a high income is a significant accomplishment, structuring your entire compensation as liquid cash presents inherent disadvantages in the long run. 🏦 This model subjects your earnings directly to the most stringent tax regulations, acting as an immediate barrier to substantial wealth creation and preservation.

Let’s dissect the stark reality of a standard cash-based compensation package:

- Core Concept: A typical professional setup where earnings are disbursed as immediate, spendable cash.

- Target Audience: Widespread among employees, mid-level managers, and corporate professionals who rely on predictable monthly paychecks.

- Taxation Impact: The entire cash sum is immediately subjected to hefty income tax rates, often the highest bracket available.

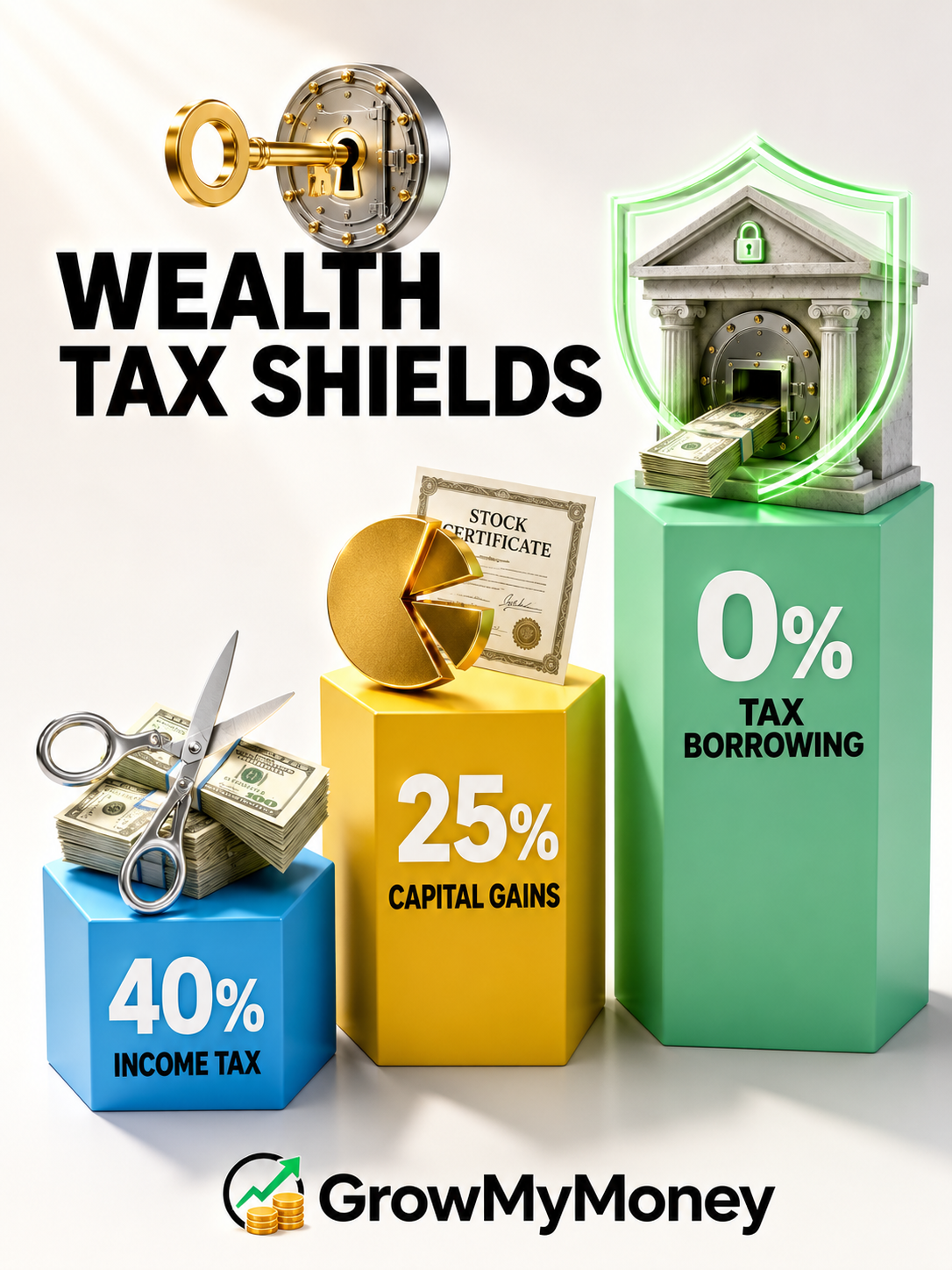

- Illustrative Scenario: Imagine a $1 Million annual salary. A typical 40% income tax rate would instantly deduct $400,000, leaving only $600,000. 📉

- Net Result: The individual is left with a significantly reduced amount of capital, hindering reinvestment and compounding potential.

This system is inherently designed to capture revenue from immediate financial transactions. When your wealth is primarily in a liquid state, the tax system takes its share before you even have the chance to strategize its growth. This forces high earners into a constant cycle of trading time for money, often missing out on the powerful effects of asset appreciation. ⏳

📈 The Equity Advantage: Shifting Towards Ownership and Deferred Taxation 💎

The paradigm shifts dramatically when individuals transition from prioritizing cash salaries to accumulating corporate equity. By negotiating compensation in the form of company stock rather than immediate currency, founders and executives become part-owners of the enterprises they help build. This strategic move alters their relationship with the tax code entirely.

When your compensation is structured as equity, you unlock a more advantageous tax framework:

- Core Concept: A strategic approach where primary compensation is received in the form of corporate shares or ownership stakes.

- Ideal for: Visionary entrepreneurs, early-stage investors, and forward-thinking executives focused on long-term asset appreciation.

- Taxation Benefit: Taxation is deferred. You only incur taxes when you voluntarily decide to sell your shares.

- Comparative Scenario: If the $1 Million worth of stock is sold, it typically incurs a capital gains tax rate, often significantly lower (e.g., 25%) than the income tax rate. This means keeping $750,000 instead of $600,000. 💰

- Enhanced Capital Preservation: By avoiding the highest income tax brackets, individuals retain an additional 15% ($150,000 per $1 Million) of their wealth. This preserved capital can be strategically reinvested, accelerating growth. 🌱

This shift to capital gains taxation offers substantial savings. However, for the truly elite, even paying capital gains tax represents a less-than-optimal outcome. The ultimate mastery lies in accessing liquidity without ever touching the principal assets, thus avoiding taxation altogether.

🛡️ The “Buy, Borrow, Die” Blueprint: Leveraging Asset-Backed Liquidity 🏰

At the zenith of sophisticated wealth management lies a powerful and legal strategy known as the “Buy, Borrow, Die” framework. This advanced blueprint allows individuals to access substantial sums of money for living expenses and investments without ever selling their appreciating assets. Instead of liquidating valuable stock to fund purchases, these assets are treated as collateral, similar to how prime real estate is used.

This ingenious method creates an ongoing stream of untaxed liquidity by keeping your wealth engine running uninterrupted:

- Core Strategy: Retain ownership of appreciating assets indefinitely while using debt as a source of immediate cash.

- Exclusive Application: Primarily utilized by ultra-high-net-worth individuals, tech titans, and leading CEOs keen on safeguarding their compounding capital.

- Tax Avoidance Mechanism: By never selling the assets, no taxable event is triggered. This means zero income tax or capital gains tax is incurred. 🚫

- Operational Example: An executive possesses $1 Million in company stock. Instead of selling, they secure a loan from a financial institution using this stock as collateral.

- Liquidity Generation: The borrowed funds are then used for daily expenses, investments, or lifestyle needs, effectively functioning as accessible income. 💳

- Legal Status: Crucially, borrowed money is not classified as income by tax authorities. Therefore, the individual reports no taxable income on their filings. ✅

- Continuous Compounding: While the loan is outstanding, the underlying stock portfolio continues to grow in value, benefiting from market appreciation. 📈

- Eventual Taxation: Capital gains tax is only incurred if and when the individual decides to sell the assets to repay the loan. In many cases, assets are held until death, with heirs inheriting them at a stepped-up basis, potentially erasing capital gains entirely. ⚰️

This elegant solution provides complete financial flexibility while ensuring that the primary wealth-generating assets remain untouched and continue to expand. Financial institutions readily offer these low-interest loans because they are fully secured by high-value corporate equity, creating a robust, self-sustaining financial ecosystem. 🌌

🌾 Building a Resilient Financial Ecosystem: Beyond Digital Assets 🌳

True financial security and long-term wealth preservation extend beyond the realm of stock portfolios and digital investments. To create an unshakeable financial foundation, it’s crucial to diversify into tangible, appreciating assets that offer stability and intrinsic value. 🔑 Think of it like building a robust digital operating system: diverse components work in harmony to enhance overall efficiency and resilience.

Integrating real-world assets into your wealth strategy provides a crucial hedge against market volatility and economic downturns:

- Tangible Asset Integration: Anchoring a portion of your capital in physical assets, such as prime real estate or productive farmland, creates a stable bedrock for your portfolio. 🏡

- Strategic Land Management: Engaging in strategic land ownership and agricultural ventures can provide consistent yields and long-term appreciation, independent of stock market fluctuations. 🌾

- Holistic Portfolio Approach: By combining the reliable returns of physical assets with the growth potential of digital investments and utilizing automated tracking systems, your portfolio transforms from a source of potential stress into a powerful engine of sustainable value creation. 📊

The journey to significant wealth is a marathon, not a sprint. It demands unwavering discipline, strategic foresight, and continuous adaptation. Always operate within the bounds of legal frameworks, and seek counsel from qualified financial and tax professionals to ensure your strategies align with current regulations and your personal financial objectives. Prioritize balancing your expenses, strategically converting surplus earnings into appreciating assets, and allowing your diversified portfolio to compound wealth safely and effectively over time. 🏁

🔗 Ready to Elevate Your Wealth Strategy? Let’s Grow Your Capital Together! 📈

Navigating the intricate landscape of advanced investment layering, asset protection, and tax minimization can seem daunting. However, you don’t have to chart this complex course alone. GrowMyMoney is committed to translating sophisticated institutional wealth strategies into actionable, high-impact habits tailored to your unique financial aspirations. 🎯 Partner with our seasoned team at GrowMyMoney today. Discover personalized asset-building blueprints, cutting-edge financial automation tools, and expert coaching designed to maximize your portfolio’s efficiency and secure your ultimate financial freedom. 🌟 Let’s build your legacy, one strategic step at a time!

❓ Frequently Asked Questions About Asset Debt and Tax Strategies ❓

Why are standard cash salaries tax-inefficient for high earners?

Standard cash salaries are highly tax-inefficient because they fall directly under the heaviest regulatory mechanisms available. Liquid paychecks are automatically hit by immediate, steep income tax rates before the capital even reaches your account, preventing optimal wealth preservation.

What is the tax rate impact on a one-million-dollar standard salary?

On a traditional salary of $1 Million, a standard 40% income tax deduction slices away a massive $400K chunk of resources, leaving the executive with a net total of only $600K in liquid capital inside their vault.

How do ultra-wealthy executives restructure their compensation?

Ultra-wealthy executives negotiate their primary compensation packages in the form of corporate stock equity rather than plain currency. This transitions them from being a temporary line-item expense into a part-owner of an expanding enterprise.

When are taxes triggered on corporate stock equity?

Taxes on corporate stock equity are deferred entirely until the asset holder makes a conscious, active choice to liquidate or sell their shares on the open market.

What is the capital gains tax advantage over income tax?

When an executive holds $1 Million in company stock and chooses to sell it, the transaction triggers a 25% capital gains tax rate instead of a 40% income tax rate, instantly saving 15% ($150K) of their total wealth.

What is the “Buy, Borrow, Die” framework?

The “Buy, Borrow, Die” blueprint is an advanced asset management strategy where ultra-high-net-worth individuals hold onto their compounding assets and use low-interest bank debt to generate cash liquidity instead of selling their shares.

How do wealthy individuals get money from banks without selling stock?

Wealthy individuals use their corporate stock portfolios as collateral to secure low-interest bank lines of credit. The bank safely extends these loans because they are fully backed by elite, top-tier corporate equity.

Why is borrowed money from an asset-backed loan not taxed?

Borrowed money from an asset-backed loan is not taxed because debt is not legally recognized or treated as real income by regulatory systems. On paper, the individual registers zero taxable income.

What happens to stock equity while it is being used as loan collateral?

While the loan remains open, the primary wealth engine is left undisturbed. The underlying corporate stocks continue to compound and appreciate in value over time on the open market.

When does an investor using asset-backed debt finally pay taxes?

The investor only triggers capital gains liabilities if and when they choose to actively sell off portions of their assets to settle the outstanding loan balance.

Is asset-backed borrowing legal for minimizing tax liabilities?

Yes. Shifting from liquid income to asset growth and utilizing collateralized lines of credit is a completely legal wealth management framework utilized within current structural regulatory codes.

How does diversified asset allocation build true financial security?

Diversified asset allocation balances your portfolio by combining digital financial markets with physical, tangible assets. This builds a resilient foundation insulated from market crashes and inflation.

What are the benefits of including physical land in a wealth strategy?

Anchoring capital into tangible, appreciating assets—such as owning land or engaging in strategic farming—creates a reliable foundation of real-world value that provides self-sustaining yields and long-term security.

Why should high earners use modern financial automation tools?

Modern financial tracking and automation applications help manage asset layering, track compounding equity growth, and monitor debt-to-collateral ratios efficiently to reduce manual management friction.

How does GrowMyMoney help individuals optimize their portfolios?

GrowMyMoney breaks down elite institutional wealth frameworks into simple, high-impact habits. We provide personalized asset-building blueprints, financial automation tools, and coaching to maximize portfolio efficiency.