Many individuals perceive financial independence as an unreachable horizon, obscured by complex jargon and volatile markets. However, the path to building substantial long-term wealth is not found in high-stakes gambling or secret investment strategies reserved for the elite. Instead, it is built upon the solid foundation of mathematical certainty and disciplined daily rituals. By shifting your focus from chasing trends to mastering core financial laws and optimizing your personal output, wealth becomes a predictable result rather than a fortunate coincidence.

The Mathematical Bedrock: Essential Financial Principles

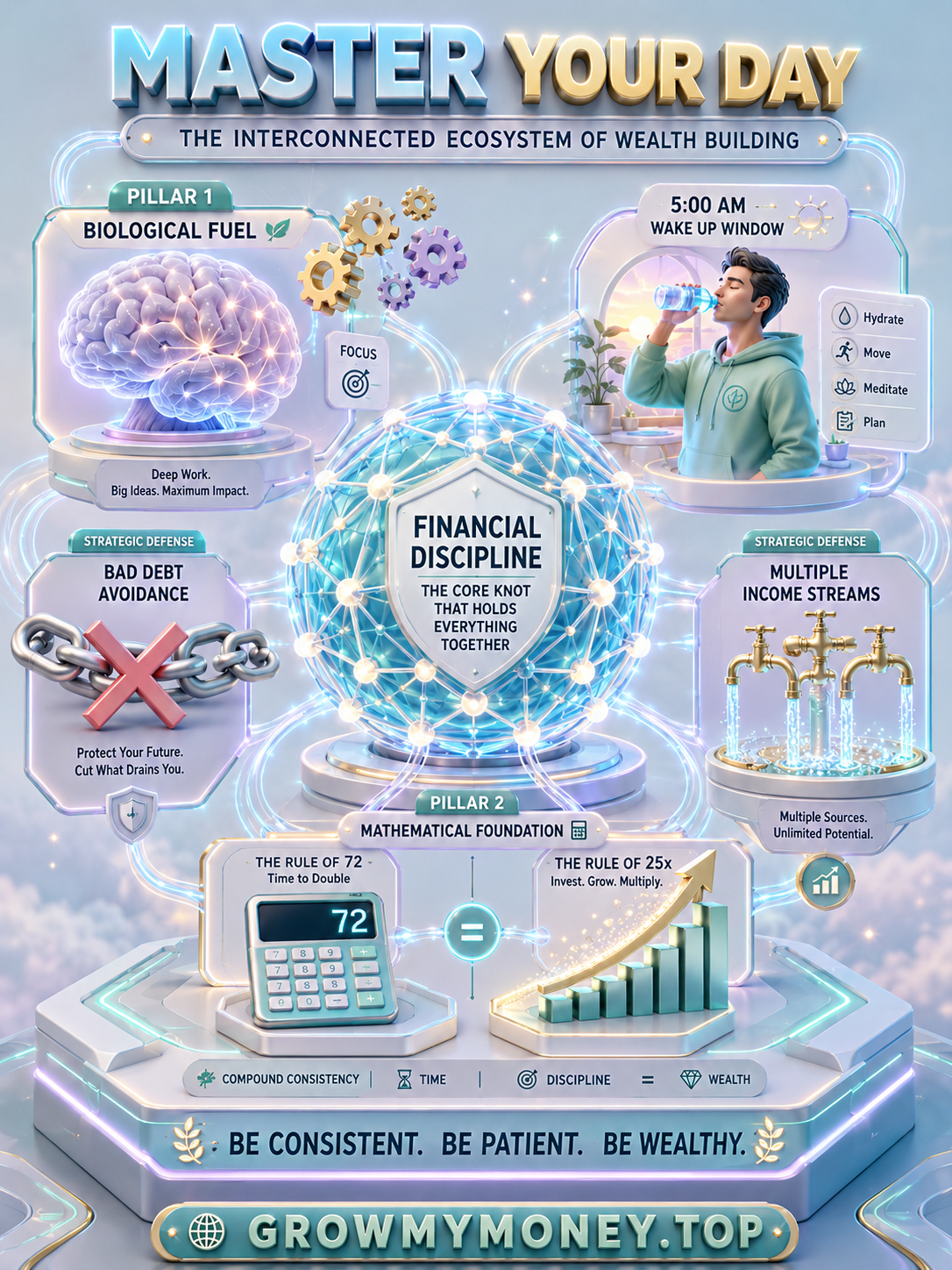

Before you can successfully grow your capital, you must understand the immutable laws of finance. These principles allow you to make rapid, logical decisions that remove the guesswork from your investment strategy.

The Rule of 72: Understanding the Velocity of Growth

The Rule of 72 is the investor’s greatest tool for visualizing the magic of compounding interest. By simply dividing 72 by your expected annual rate of return, you arrive at the approximate number of years required for your initial capital to double. For example, if your portfolio achieves an annual return of 8%, your money will double in just nine years. This understanding is critical; it teaches you why chasing 2% savings accounts is a losing game and why long-term investing is the true engine of wealth creation.

The Rule of 25x: Defining Your Financial Freedom

What is your endgame? The Rule of 25x provides a clear, actionable target for retirement. To calculate your financial freedom number, determine your total annual expenses and multiply that figure by 25. Once your total invested assets reach this amount, you are statistically capable of sustaining your lifestyle through market returns alone, effectively freeing your time from the necessity of labor. This creates a concrete objective that transforms vague goals into a measurable race against time.

Disciplined Consumption: The 20/4/10 Guideline

Lifestyle creep is the silent killer of wealth. When purchasing depreciating assets like vehicles, utilize the 20/4/10 rule: provide a 20% down payment, restrict the loan duration to no more than 4 years, and ensure total monthly vehicle costs do not exceed 10% of your gross income. By adhering to these guardrails, you prevent your monthly cash flow from being eroded by unnecessary debt, keeping your wealth-building engine running at full capacity.

Structuring Your Day for High-Performance Wealth

Your financial outcomes are a direct reflection of your cognitive energy and focus. To grow your net worth, you must treat your time as a finite, high-value asset. Creating a structured routine is not about restriction; it is about maximizing the hours in your day.

The Morning Architecture (5:00 AM – 11:00 AM)

The early morning hours are the most critical for high-stakes decision-making. By waking up between 5:00 and 7:00 AM, you align your biological clock with the natural day. Use the hours between 9:00 AM and 11:00 AM for ‘Deep Work.’ During this cognitive peak, your brain is best equipped to handle complex investment research, strategy formulation, or creative problem-solving. This is when you should tackle your most challenging tasks rather than wasting mental bandwidth on trivial emails or administrative maintenance.

The Afternoon Pivot and Recovery

Energy naturally fluctuates throughout the day. Recognize the ‘afternoon dip’—typically occurring after lunch—as a time for lower-intensity tasks. To sustain peak performance, prioritize physical activity in the early evening. Strength training or cardiovascular exercise not only enhances physical health but also reinforces the mental resilience required to weather market volatility.

The 25 Essential Habits of Wealth Builders

Grand gestures do not build legacies; consistent, small habits do. To engineer wealth, incorporate these behaviors into your lifestyle:

- Pay Yourself First: Before settling bills, allocate a portion of your income to investments. Treat this as a non-negotiable debt to your future self.

- Avoid Bad Debt: Differentiate between productive leverage and consumer debt. Avoid high-interest loans for assets that lose value.

- Continuous Education: Your greatest asset is your ability to earn. Devote time to reading, attending seminars, and developing new professional skills.

- Curate Your Circle: You are the average of the people you interact with most. Surround yourself with individuals who value growth, financial literacy, and ambition.

- Automate Savings: Use technology to remove human error from your savings strategy. If it is automatic, it becomes inevitable.

Adopting the Mindset of a CEO

Managing wealth requires a shift from an employee mentality to an executive one. True wealth builders treat their personal life with the same strategic rigor as a successful corporation.

Emotional Intelligence (EQ) in Investing

Markets are driven by the collective psychology of fear and greed. An investor with high EQ remains calm when others are panicking and disciplined when others are being lured by speculative hype. Mastering your own emotional responses is the ultimate competitive advantage in the financial markets.

Visionary Thinking

The ability to project your decision-making into the next decade—rather than the next week—is what separates those who build lasting wealth from those who stay trapped in a cycle of short-term survival. When you prioritize long-term outcomes, the day-to-day noise of market fluctuations loses its power over your nerves.

Accountability and Integrity

Taking full ownership of your financial current state is the first step toward changing it. Do not look for scapegoats in the economy or your employer. Furthermore, maintain uncompromising integrity. In the world of high-level finance, your reputation is your most valuable currency; protect it by ensuring your actions are always aligned with your stated values.

The Reality of the Long Game

Wealth building is fundamentally a game of patience, rules, and logic. Avoid the allure of ‘get-rich-quick’ schemes that promise high returns with low effort—they are universally traps. Instead, rely on the five fundamental pillars:

- Use Rules: Standardize your decision-making processes to avoid analysis paralysis.

- Eliminate Emotional Spending: Question every purchase. Is it a reflection of your goals, or is it merely an attempt to satisfy temporary validation?

- Focus on the Math: Trust the numbers, the compound interest tables, and the data. Headlines are designed to provoke; numbers are designed to inform.

- Maintain Unwavering Consistency: The greatest wealth is built by the boring, steady application of the same habits over decades.

- Leverage the Power of Time: Start now. The single most important variable in the compounding equation is the duration of your investment timeline.

Final Thoughts: Your Journey Begins Today

Financial independence is not a destination reserved for the lucky; it is the inevitable outcome of a life managed with precision. By waking up earlier, controlling your expenses, investing in your own skill sets, and adhering strictly to the Rule of 72 and the Rule of 25x, you are effectively buying your future freedom. Remember, the best time to plant the tree was twenty years ago; the second best time is today. Take the first step by auditing your expenses, setting your freedom number, and automating your first investment. Your future self will thank you for the discipline you display today.

Frequently Asked Questions (FAQ)

What is the Rule of 72 in wealth building?

The Rule of 72 is a mental shortcut to estimate how long it will take to double an investment. Divide 72 by your annual interest rate. For instance, at a 6% return, your money doubles every 12 years.

How do I calculate my financial freedom number using the Rule of 25x?

Multiply your total annual expenses by 25. This provides a baseline target for the amount of invested assets required to cover your living costs annually, allowing you to live off your portfolio safely.

What is the 20/4/10 rule for purchasing a vehicle?

This rule ensures you don’t overspend on transportation: put at least 20% down, finance for no more than 4 years, and ensure total monthly payments stay at or below 10% of your gross monthly income.

Why should I prioritize paying myself first?

Paying yourself first ensures that savings are a priority, not an afterthought. It automates the wealth-building process and prevents you from spending what should have been allocated for your future.

How can I avoid emotional spending?

Implement a ‘waiting period’ for all non-essential purchases. If you want something, wait 48 hours. Often, the urge to spend will fade, and you will make a more logical decision.

Is it better to focus on high-yield investments or reducing expenses?

Both are critical, but reducing expenses provides immediate, guaranteed capital for investment. Focus on increasing your savings rate first, then optimize the yield on your capital.

How does waking up early help with money?

It provides a ‘protected’ window of time before the chaos of the day begins, allowing for better planning, learning, and focused work on high-ROI activities.

What constitutes ‘bad debt’?

Bad debt consists of high-interest obligations for items that depreciate rapidly, like consumer electronics or luxury goods, which do not offer any future financial return.

What role does emotional intelligence play in finance?

EQ helps you avoid panic-selling during market crashes and prevents you from buying assets out of fear of missing out (FOMO). It keeps your strategy objective.

How do I start building wealth if I have very little to invest?

Start with the habit of saving a small percentage of your income regardless of the amount. The discipline is more important initially than the dollar figure, as it builds the momentum needed for larger future investments.