Have you ever felt like a hamster on a wheel? You show up to work every day, labor for hours, collect your paycheck, and watch it vanish almost instantly into the maw of monthly expenses. This cycle of working to survive is a trap that ensnares millions of people across the globe. The tragic irony is that for many, this struggle isn’t necessarily a result of a low income; it is the inevitable consequence of a specific psychological framework: the “broke mindset.”

The Psychology of Financial Limitation

Many believe that wealth is a matter of luck, inheritance, or having the right job. While those factors certainly play a role, the foundation of lasting prosperity is built entirely on how one thinks about money, time, and value. Transitioning from a state of constant financial stress to a state of abundance requires a total dismantling of the habits that hold you back.

If your goal is to break free from the invisible barriers of the middle-class trap, you must stop viewing your life through the lens of scarcity. It is time to replace your old, reactive financial habits with a proactive, architect-level strategy designed to generate long-term growth.

Mastering the Wealthy Cash Flow Protocol

The most significant indicator of your financial future is not your bank balance today; it is the path your money takes the moment it touches your account. If you want to change your trajectory, you must master the mechanics of capital flow.

The Scarcity Loop

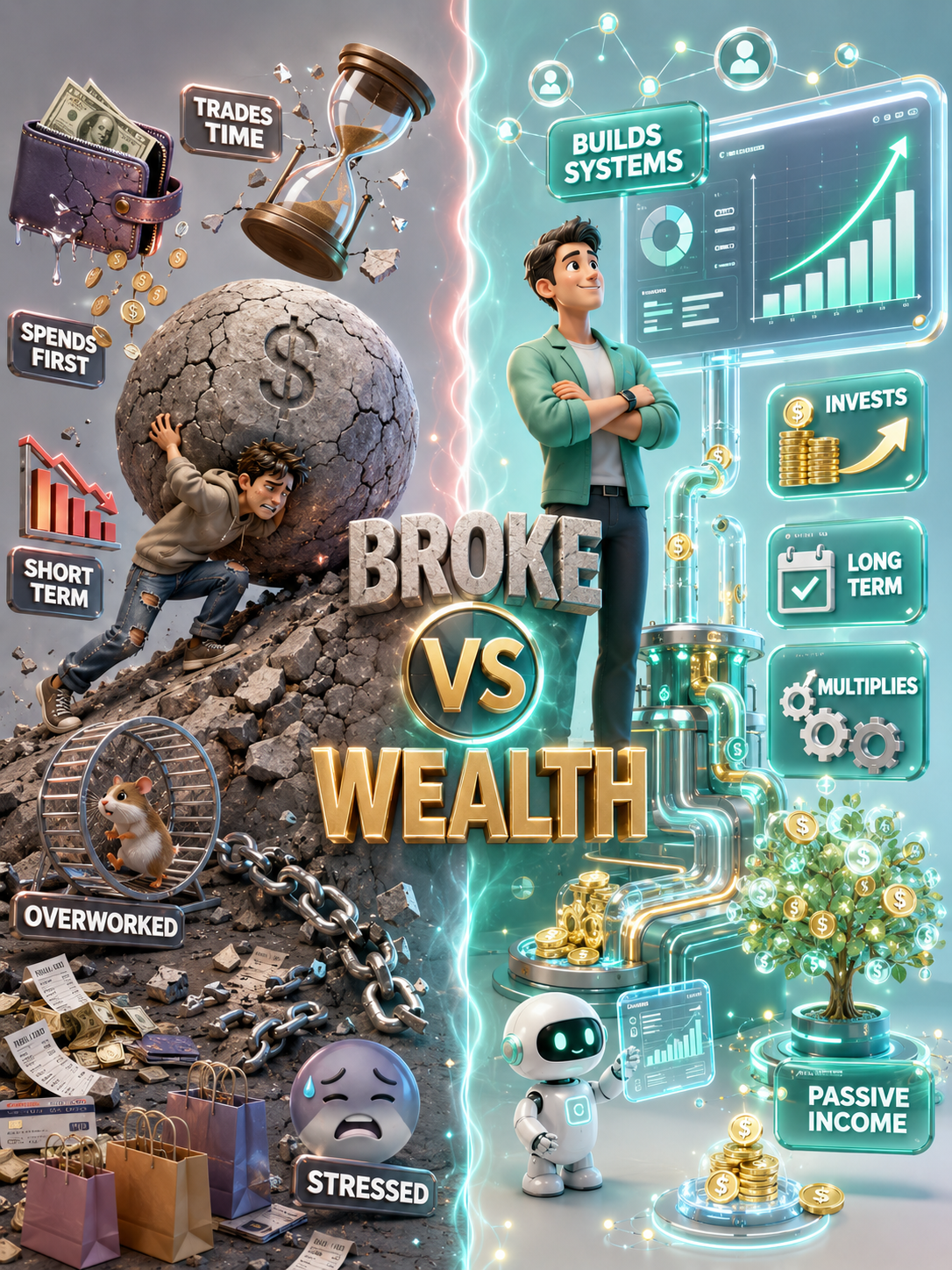

Most individuals operate under the “Spend-First” model. They receive a paycheck, immediately deduct their living expenses and lifestyle costs, and hope that something remains for savings. Because human nature dictates that we will always expand our spending to match our income, this usually leads to an account balance of zero by the end of the month. In this scenario, you are always one emergency away from personal financial collapse.

The Wealthy Protocol

The wealthy do not treat their paycheck as an allowance for consumption. They treat it as a seed for growth. Their protocol is simple but requires immense discipline:

- The Intake: Generate revenue through labor or business operations.

- The Interception: Before the first bill is paid, a set percentage of that income is immediately diverted into investment vehicles.

- The Deployment: This capital is funneled into assets—not liabilities—that produce their own income.

- The Result: Over time, the income produced by these assets eventually eclipses the need for manual labor.

Prioritizing Assets Over Ego-Driven Consumption

If you examine your current personal ledger, you might find that much of your wealth has been traded for depreciating items. Society is structured to push us toward consumption—shiny new smartphones, high-end fashion, and luxury vehicles that lose value the moment they leave the showroom floor. Every dollar spent on these items is a dollar that could have been working for you.

A true wealth builder understands the difference between an asset and a liability. An asset puts money in your pocket; a liability takes money out. To build real wealth, you must shift your focus toward:

- Real Estate: Properties that generate consistent monthly rent.

- Dividend-Paying Equities: Stocks in profitable companies that share their earnings with you.

- Scalable Businesses: Ventures that can operate independently of your direct daily involvement.

The next time you are tempted by an impulse purchase, ask yourself a critical question: “Does this item contribute to my future freedom, or is it simply a temporary dopamine hit?”

The Time-Money Decoupling Strategy

Time is the only resource that is strictly finite. If your income is strictly tied to the hours you clock in, you will always face a “ceiling” on your earnings. If you get sick, take a vacation, or simply burn out, your income stops. This is the ultimate trap of the working class.

Wealthy individuals view time differently. They aim to disconnect their earnings from their physical presence. They do this by building systems. Whether it is an automated software product, an e-commerce brand, or a rental property management system, the objective is to build something that functions while you sleep. When you own a system, you are no longer selling your hours; you are selling your capacity to innovate and manage.

The Strategic Use of Debt as Leverage

Debt is often vilified, but in the hands of the financially literate, it is a powerful tool. The difference lies in whether you use debt for consumption or acquisition.

Using a credit card to pay for a vacation is consumer debt—it is a weight around your neck that provides no future return. Conversely, using a bank loan to purchase a cash-flowing real estate property is strategic leverage. In the latter, you are effectively using the bank’s capital to buy an asset that pays its own monthly loan installment via rental income, while you retain the remaining profit. This is the secret to scaling wealth far faster than saving alone could ever achieve.

The Golden Rule of Priority: Pay Yourself First

Parkinson’s Law warns us that our expenses will rise to meet our income level unless we impose external constraints. The solution is to flip the formula. Instead of budgeting what is left over, you should budget the portion you are keeping for your future self first.

Automation is your best friend here. By setting up an automatic transfer that pulls 15% to 20% of your income into an investment account the day you get paid, you remove the “willpower” element from the equation. You adjust your lifestyle to fit the remaining funds, and before you know it, you are building wealth on autopilot. This is not just a habit; it is a mathematical strategy for success.

Conclusion: Engineering Your Freedom

The transition from a survival mentality to a wealth-building one is a process of identity transformation. You must stop identifying as someone who works for a paycheck and start identifying as someone who owns systems, manages capital, and prioritizes long-term outcomes over short-term gratification.

True financial freedom is not about the size of the pile of money you have sitting in a vault; it is about the ability to control your own time and influence your own future. If you are tired of living in the shadow of month-to-month survival, take the first step today. Automate your savings, eliminate toxic consumer debt, and begin acquiring assets that will work for you for years to come. Your financial destiny is not a result of your past; it is the sum total of the decisions you make starting right now.

Frequently Asked Questions

What is the primary distinction between a broke mindset and a wealth mindset?

The broke mindset centers on survival, immediate gratification, and spending everything one earns. The wealth mindset focuses on long-term growth, asset acquisition, and the strategic delay of gratification to create lasting financial freedom.

How should a person change how they view their monthly paycheck?

Stop viewing a paycheck as money to spend. Instead, see it as a resource to be allocated. A portion should always be “intercepted” for investments before any bills or luxury purchases occur.

What does it mean to “pay yourself first”?

It means prioritizing your savings and investments immediately upon receiving income. By automating this, you treat your own financial growth as your most important “bill,” ensuring that you are consistently building wealth rather than just paying creditors.

Why is trading time for money a limitation?

Because time is finite, your income potential will always be capped by the number of hours you can work. To achieve true wealth, you must move toward business models and investments that generate money independently of your presence.

How can I decouple my time from my income?

Focus on building systems. This could be creating digital content, investing in dividend-paying stocks, or purchasing real estate. These assets continue to generate value whether you are at your desk or asleep.

What is the difference between “good” debt and “bad” debt?

Bad debt is used for consumption, such as high-interest credit cards for retail items. Good debt is used as leverage, such as a mortgage for a property that will be rented out to generate positive cash flow.

How does Parkinson’s Law affect my finances?

Parkinson’s Law suggests that your expenses will always rise to consume your entire income. If you get a raise and don’t intentionally increase your savings rate, you will likely end up with the same level of stress, just with a more expensive lifestyle.

Is it necessary to be wealthy to start building wealth?

Absolutely not. You build wealth through consistent habits and small, disciplined investments over long periods of time. The mindset comes first, and the wealth follows.

What is the ultimate goal of the wealth mindset?

The goal is to move beyond mere survival into a life of abundance where your income is generated by your assets, allowing you complete freedom to choose how you spend your time and energy.

Can I change my mindset if I am currently struggling?

Yes. Mindsets are developed through habits. By starting with small, consistent actions—like automating a tiny portion of your income into an investment—you begin to prove to yourself that you are in control of your financial future.