True financial prosperity is rarely the result of a singular, lucky windfall or the byproduct of working yourself to the bone without a strategy. Instead, enduring wealth is meticulously constructed through the architecture of your habits, the clarity of your vision, and the intentionality of your daily decisions. Many people find themselves trapped in a cycle of financial struggle, often unaware that they are operating under the weight of inherited limiting beliefs and outdated money behaviors. The most exciting realization? You can rewrite your financial destiny by making specific, strategic shifts in your perspective.

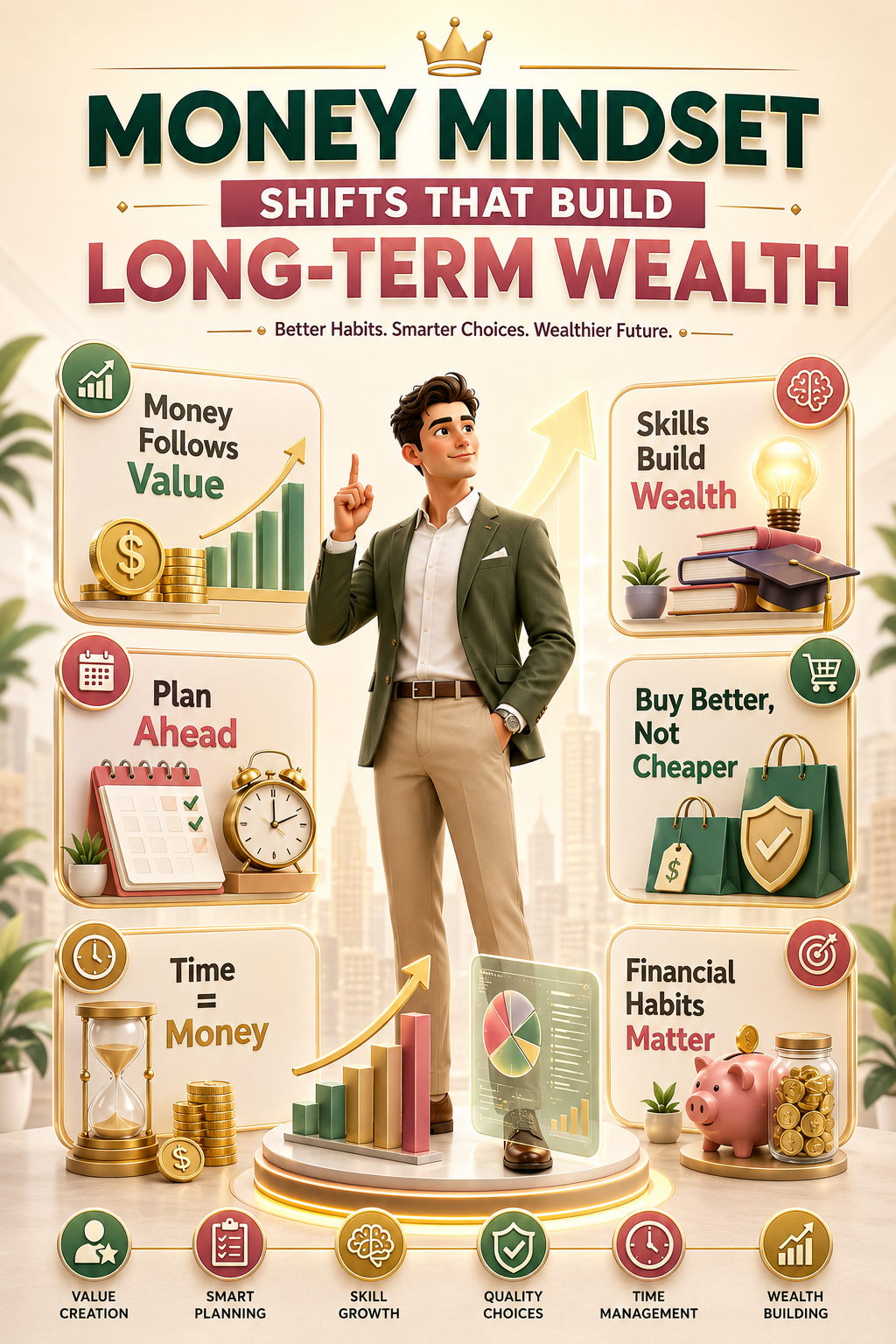

1. The Shift from ‘Working Hard’ to ‘Creating Value’

There is a dangerous misconception that financial success is strictly a linear function of how many hours you put into your job. While effort is foundational, exhaustion is not a strategy. If your primary path to wealth is trading time for money at a fixed rate, you will always face a ceiling. Wealth builders understand that income is a byproduct of the value they provide to the marketplace.

To scale your finances, you must transition your focus toward solving more complex problems. Whether you are an entrepreneur, a freelancer, or a high-level employee, the goal should be to position yourself where your unique skills generate exponential outcomes rather than incremental ones. Ask yourself: Are my current efforts building a system that serves me, or am I just feeding the system?

2. Breaking Free from Inherited Financial Patterns

We often carry the “financial DNA” of our parents and early environment. If you grew up in a household where money was a source of fear, debt, or scarcity, those internalized beliefs likely dictate your current spending or saving habits. Many people suffer from “financial autopilot,” where they react to money based on subconscious programs set decades ago.

To break the cycle, you must practice radical financial self-awareness. Identify your triggers. Do you spend impulsively when stressed? Do you hoard cash out of deep-seated anxiety? By shining a light on these inherited patterns, you can consciously choose to replace them with rational, goal-oriented behaviors. This is the first step toward true financial autonomy.

3. The Superiority of Skills Over Fleeting Trends

In the digital age, we are constantly bombarded by “get-rich-quick” trends—the latest crypto craze, the newest dropshipping model, or the hot stock of the week. While these might offer short-term excitement, they rarely offer long-term security. The wealthiest individuals invest heavily in what remains constant: their ability to solve problems.

Cultivating high-value, durable skills—such as advanced negotiation, persuasive communication, analytical thinking, or technical proficiency—provides a hedge against economic volatility. Trends will come and go, but the capacity to adapt and innovate remains a lifelong asset that continuously appreciates. Invest in your brain before you invest in your portfolio; the ROI on education is consistently higher than any market speculation.

4. Rethinking ‘Value’: Why Cheap Costs More

A scarcity mindset tricks us into believing that the lowest price tag is the smartest financial move. This is the “false economy” trap. When you prioritize the absolute lowest cost over quality, you often end up replacing items more frequently, dealing with maintenance headaches, and settling for suboptimal performance. This habit of buying ‘cheap’ can drain your resources slowly over a lifetime.

Financially successful people adopt the long-term cost principle. They analyze the cost-per-use and the longevity of an item. Whether it is professional tools, home appliances, or even personal services, paying a premium for quality is often an investment in both durability and mental peace. Stop counting the immediate cash outflow and start calculating the long-term value.

5. Time Management is Wealth Management

Time is the only asset that, once spent, can never be recovered. The relationship you have with your calendar is a direct indicator of your future wealth. If you are constantly reactive—putting out fires, paying late fees, or ignoring your financial planning—you are losing money by the minute.

Effective wealth builders view their time as capital. They allocate time for deep thinking, financial review, and strategic planning. They don’t just ‘get to it when they can’; they treat their finances as a business that requires regular audit and maintenance. By scheduling your financial growth, you reduce the chaos that leads to impulsive spending and missed opportunities.

6. Budgeting as a Tool for Freedom, Not Restriction

A common mistake is viewing a budget as a cage. This perception often leads to rebellion against one’s own financial health. Instead, shift your mindset to view a budget as a map. A map does not restrict your travel; it ensures you arrive at your desired destination without getting lost in the woods.

When you track your expenses, you aren’t limiting yourself; you are ensuring that your money is flowing toward the things that truly align with your long-term vision. Without a budget, you are a passenger in your own life. With one, you are the pilot. Tracking your cash flow provides the clarity needed to make confident, guilt-free decisions about your spending.

7. The Power of Consistent, Compound Action

We often underestimate what we can achieve in a decade while overestimating what we can do in a year. The most effective wealth-building strategies are boring. They don’t make headlines. They involve setting up automatic savings, investing consistently regardless of market sentiment, and incrementally increasing your earnings over time.

Real wealth is built in the quiet moments between the “big breaks.” It is built in the small, consistent decisions to prioritize saving over spending, learning over entertainment, and discipline over comfort. These micro-shifts in daily behavior compound over time, creating a tidal wave of financial momentum that eventually becomes unstoppable.

Final Thoughts: Shaping Your Future

Your financial situation today is the harvest of the habits you planted yesterday. If you are unsatisfied with the yield, you must change the seeds. By embracing these seven mindset shifts, you are doing more than just managing money—you are cultivating a life of financial agency. Wealth is not a destination; it is a way of operating. Start today, remain consistent, and let the quiet power of these habits build the foundation for a future of abundance.

Frequently Asked Questions (FAQ)

1. Why is financial mindset important?

Financial mindset influences your daily spending habits, saving behavior, investing decisions, and your ability to bounce back from economic setbacks.

2. Can I change my financial habits if I’ve had them my whole life?

Absolutely. While deeply ingrained, financial behaviors can be transformed through intentional awareness, ongoing education, and consistent practice.

3. Why do professional skills matter more than investment trends?

Your skills are your primary engine for generating income. Markets are volatile and trends change, but a highly skilled individual remains valuable regardless of the economic climate.

4. Is budgeting truly necessary for someone with a high income?

Yes. Without budgeting, even high earners often suffer from ‘lifestyle creep,’ leading to high spending despite high income, which prevents true wealth accumulation.

5. How can I start building an emergency fund if I have limited cash?

Start small. Even saving a tiny percentage of your income consistently creates a habit. The goal is to build the muscle of saving before worrying about the size of the initial deposit.

6. Does buying quality really save money?

Yes. When you purchase high-quality items, they last longer and perform better, reducing the ‘replacement cost’ that plagues those who consistently buy the cheapest available options.

7. How do I overcome the fear of investing?

The fear usually stems from a lack of knowledge. Start by educating yourself on simple, long-term index fund strategies rather than trying to beat the market with individual stocks.

8. What is the biggest mistake people make regarding money?

The biggest mistake is the lack of a long-term plan. Many people live for the ‘next paycheck’ without ever directing their money toward specific, future-oriented goals.

9. How does time management correlate with wealth?

Effective time management allows you to focus on high-leverage activities that increase your earning potential and reduce the costly errors that arise from rushing.

10. Can anyone achieve long-term wealth?

Yes. While starting points differ, the principles of living below your means, increasing your value, and investing for the long term are universally effective strategies for wealth creation.