For millions of individuals, the cycle of life feels like a high-speed treadmill: you work exhausting hours, receive a paycheck, and watch that money evaporate into bills and monthly living expenses before the next cycle begins. This is the hallmark of the “survival loop.” If you feel trapped in this perpetual cycle of earning and spending, it is time to face a difficult truth: your financial situation is not merely a consequence of your salary, but a reflection of your underlying psychological framework regarding money.

The Psychology of Prosperity

Transitioning from a broke mindset to a wealthy one requires more than just a desire for more cash; it demands a radical overhaul of your daily financial conduct. While the average person views money as a commodity to be consumed, the wealthy view it as a seed to be planted. To break free from the invisible chains of mediocrity, you must dismantle the habits that keep you tethered to a paycheck and adopt a new system of capital management.

Wealth is not just about the numbers in your bank account—it is about the systems you build to ensure those numbers grow without your constant, direct labor. Let’s explore the essential shifts required to move from the state of constant financial anxiety to a position of generational security.

The Wealthy Cash Flow Protocol

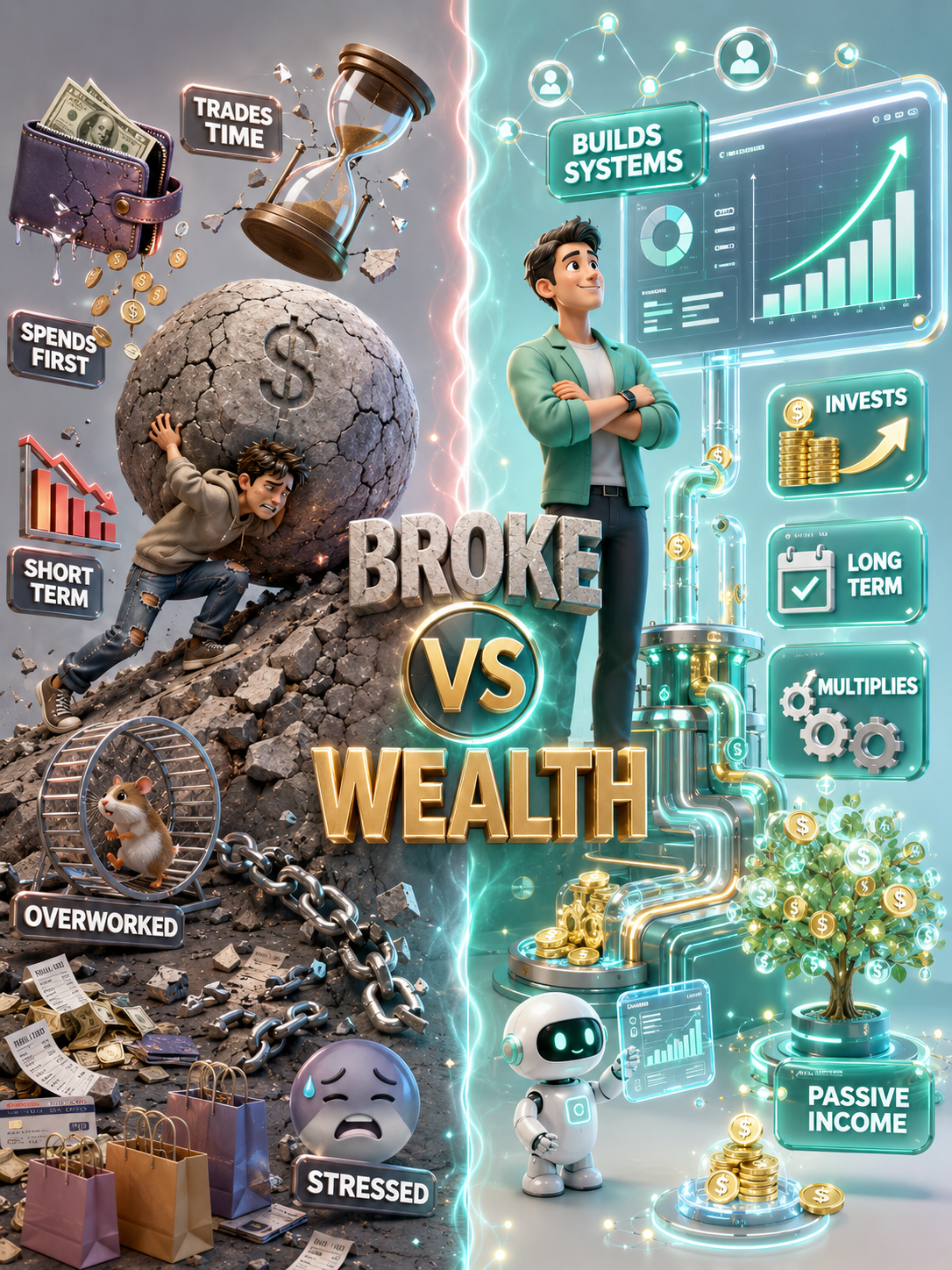

The primary divider between those who struggle and those who thrive is the trajectory of their cash. If your money enters your account and flows directly out to retailers, restaurants, and credit card companies, you are funding everyone else’s prosperity but your own.

The Broke Formula: Earn → Spend → Save (if there is anything left). This is a recipe for disaster, as human nature dictates that expenses will always expand to consume available funds.

The Wealthy Formula: Earn → Invest → Spend. Those who build wealth treat their investment contributions as their most important “bill.” By intercepting a significant portion of their income before it ever touches their discretionary spending, they guarantee that their net worth grows every single month, regardless of what the economy does.

The Trap of Perceived Wealth vs. Actual Ownership

Our culture is obsessed with signaling. Many people fall into the trap of spending their future capital on items that lose value the second they are removed from the store shelf. Whether it is the latest smartphone, a luxury vehicle, or designer apparel, these purchases act as financial anchors. They provide a temporary dopamine rush but do absolutely nothing to increase your financial security.

A wealth-oriented mindset focuses exclusively on ownership. Instead of buying goods that depreciate, the affluent investor prioritizes assets that appreciate or produce cash flow. This includes:

- Real Estate: Properties that generate monthly rent, providing consistent cash flow while building equity.

- Dividend-Paying Equities: Owning portions of profitable companies that share their gains with shareholders.

- Business Systems: Creating or acquiring entities that operate independently, providing revenue even while the owner is away.

Decoupling Time from Income

One of the most dangerous myths in modern labor is that you must trade hours for dollars. If your income is strictly tied to your physical presence, you have placed a hard cap on your earning potential. You only have twenty-four hours in a day, and you need sleep, food, and rest. If you are not working, you are not earning.

Wealthy individuals understand that true freedom comes from systems. They dedicate their energy to creating assets that scale. A digital product, an automated investment portfolio, or a business system functions while you sleep. These systems do not require your hourly participation to deliver value. By building these engines of income, you escape the biological limits of the human body and move toward true time freedom.

Strategic Debt: The Tool of the Financially Literate

There is a fundamental difference between “good debt” and “bad debt.” The average consumer uses debt to fund their lifestyle—taking out high-interest loans for vacations or consumer electronics. This is economic suicide, as it forces you to pay interest on items that provide no return.

Conversely, the wealthy use debt as a form of leverage. By securing a low-interest loan to purchase a revenue-generating asset, they allow the asset to pay for the debt. In this scenario, the bank provides the capital, the tenant provides the rent, and the owner keeps the equity and the cash flow. When used properly, debt is not a shackle; it is a ladder that accelerates your path to financial independence.

Applying Parkinson’s Law to Your Benefit

Parkinson’s Law states that “work expands so as to fill the time available for its completion.” In finance, this translates to expenses expanding to meet your income. This is exactly why a raise rarely results in more savings. To combat this, you must automate your wealth creation.

By automating the transfer of a percentage of your paycheck directly into investment vehicles, you force your lifestyle to adjust to the remaining capital. It is a form of self-imposed constraint that forces efficiency. If you don’t see the money, you don’t miss the money. This simple shift in automation turns wealth building from an exercise in willpower into a mathematical certainty.

Defining Your Ultimate Goal: Freedom

Why do you want to be wealthy? If the goal is simply to have a high balance, you will likely remain stressed. The true goal of a wealth mindset is freedom. Freedom is the ability to choose how you spend your day, who you spend it with, and where you live. It is the ability to disconnect your survival from your daily labor.

When you stop focusing on “how can I afford this?” and start asking “how can I build a system that pays for this?”, you have officially shifted your mindset. You are no longer a servant to your finances; you are the architect of your destiny.

Taking the First Step

The bridge between where you are today and where you want to be is built with small, consistent actions. You do not need a massive windfall or a lottery win to start; you need a change in behavior. Start by auditing your current spending, identifying one luxury you can cut to fund an asset purchase, and automating your savings.

The journey to wealth is not a sprint; it is the result of years of disciplined, strategic choices. Each dollar you invest today is a soldier in your army of wealth, working for you indefinitely. Stop looking for shortcuts and start focusing on the fundamental pillars of asset ownership, system creation, and disciplined capital allocation.

Your financial future is waiting for you to take command. Will you continue to chase a paycheck, or will you start building the systems that will provide for you and your family for generations to come? The choice is made with every single transaction you authorize. Make the right one today.

Frequently Asked Questions

What is the core difference between a broke mindset and a wealth mindset?

A broke mindset is reactive, focused on immediate consumption and survival. A wealth mindset is proactive, focused on the long-term accumulation of assets and the creation of passive income streams.

How does a wealthy mindset treat a monthly paycheck?

Instead of viewing a paycheck as spending money, the wealthy view it as capital. They immediately allocate a portion to investments before addressing living expenses, ensuring growth occurs before consumption.

What does ‘paying yourself first’ mean?

It means prioritizing your future self by moving a set percentage of your income into savings or investments immediately upon receiving it, rather than waiting to see what is left at the end of the month.

Why is trading time for money considered a trap?

Because time is a finite resource. When your income is tied to your hours worked, your earning potential has a ceiling, and your income stops the moment you stop working.

How do the wealthy decouple their time from income?

They create or buy systems—such as businesses, rental properties, or automated portfolios—that continue to function and generate profit regardless of their direct daily involvement.

What is the difference between a cash-flowing asset and a luxury?

A cash-flowing asset (like a rental home or stock) earns you money over time. A luxury item (like a sports car) requires ongoing maintenance and depreciates in value, costing you money.

Is all debt detrimental to my wealth?

No. ‘Bad debt’ is used for consumption (credit cards for shopping). ‘Good debt’ is used for leverage (loans for investment properties) where the asset’s return exceeds the cost of borrowing.

What is the best way to start building wealth with a limited income?

Focus on reducing your recurring expenses to free up cash, prioritize financial education, and start by investing even small, consistent amounts to take advantage of compound interest.

What is Parkinson’s Law, and how does it affect my finances?

Parkinson’s Law suggests that your spending will rise to match your income. To overcome this, you must set up automatic transfers for investments so your expenses don’t consume your raises.

What is the ultimate goal of adopting a wealth mindset?

The ultimate goal is time freedom—the ability to live life on your terms without being forced to work for your survival.