Most people fall into the trap of believing that financial independence is reserved for those who hit the jackpot, climb to a C-suite executive position, or inherit a fortune. There is a prevailing myth that the only way to escape the rat race is to earn a massive salary. However, the reality of wealth creation is far more mundane—and far more accessible. Genuine financial stability is almost always the result of incremental, daily habits executed with unwavering consistency over several years.

When you shift your focus from chasing the “next big win” to refining the small, daily financial choices you make, you transform your relationship with money. From streamlining your subscription services to automating your investment contributions, the smallest decisions carry the most weight when viewed through the lens of compound interest and long-term momentum.

The Myth of the “Big Financial Break”

The human brain is wired to crave instant gratification and massive milestones. We celebrate the promotion, the bonus, or the unexpected windfall. Yet, history shows that massive income spikes often lead to “lifestyle creep” rather than long-term security. If you haven’t mastered your daily habits, a higher salary simply becomes a larger pool of money to lose to bad habits.

Real financial architecture is built on a foundation of intentionality. It is about understanding the flow of money into and out of your life. By focusing on small habits, you aren’t just saving pennies; you are building a system that functions independently of your willpower. When you move from passive consumption to active financial management, you regain control over your future.

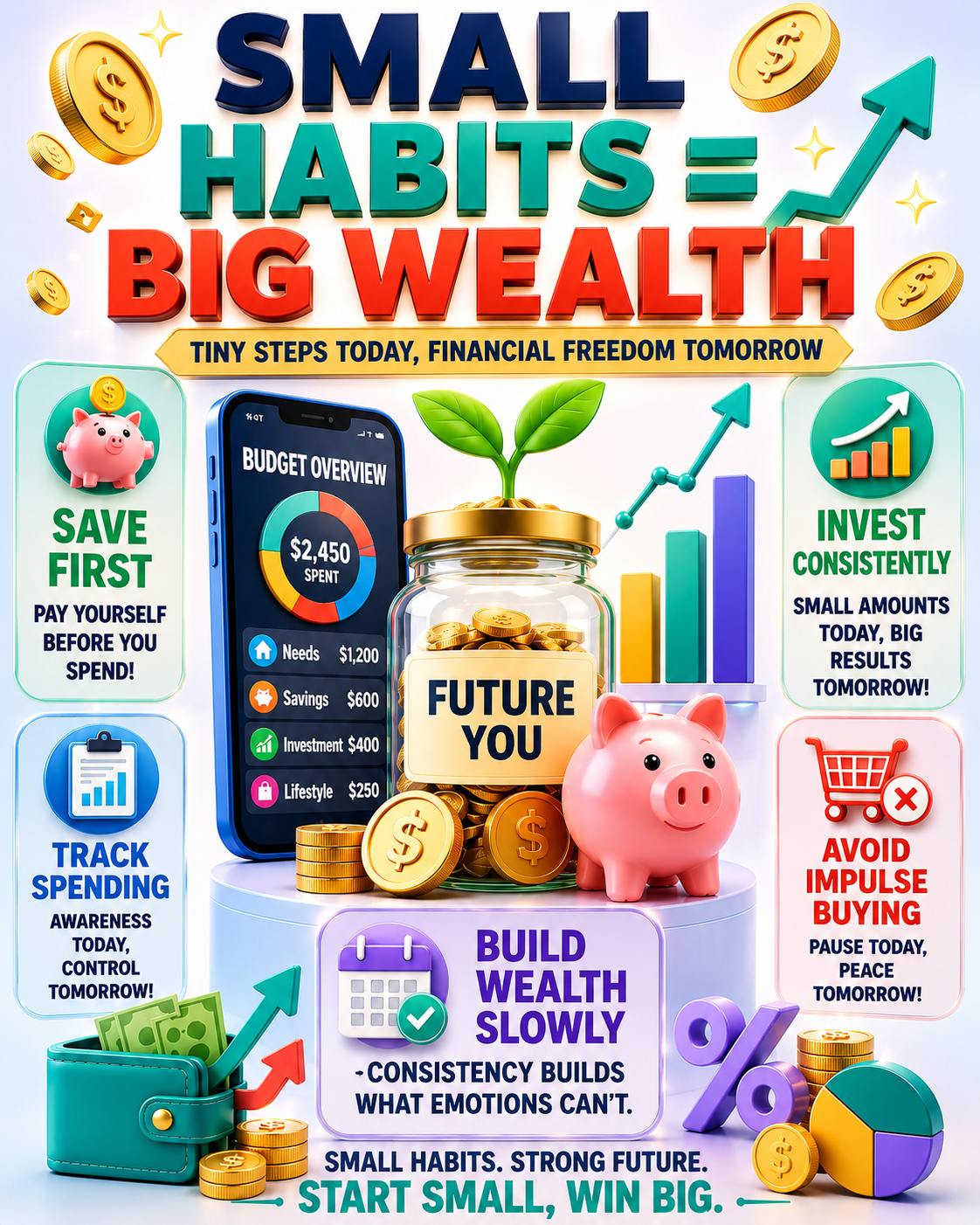

Mastering the “Save First, Spend Later” Philosophy

The most dangerous financial mistake most people make is treating their savings as a residual activity. Many wait until the end of the month, looking at what is left in their checking account, and then deciding how much to put into savings. In an economy designed to encourage spending, there is rarely anything left.

To break this cycle, you must reverse the equation: Save first, spend what remains. When you treat your savings contribution like a non-negotiable “bill” that must be paid at the start of each month, your spending habits naturally adapt to your available cash flow. By automating this transfer—sending money from your paycheck directly into a high-yield savings or investment account—you bypass the psychological pain of “losing” money, because you never see it sitting in your primary spending account.

The Clarity Provided by Expense Tracking

You cannot manage what you do not measure. Many individuals live in a state of financial fog, unaware of how their recurring daily expenses accumulate. Tracking your spending is not about deprivation; it is about visibility. When you see where your capital is leaking—whether it is through unused streaming subscriptions, excessive dining out, or impulse digital purchases—you can plug those holes.

Start by auditing your accounts for the last 90 days. Categorize every dollar. You will likely find “phantom expenses” that add no actual value to your quality of life. Once these are eliminated, that capital can be redirected toward debt reduction or investment vehicles where it can begin to compound.

The Silent Erosion: Managing Impulse Purchases

The digital age has made spending easier than ever. One-click checkouts, personalized social media ads, and constant flash sales are designed to bypass your logical decision-making process. To combat this, you need to introduce friction into your shopping process.

Implement a mandatory waiting period. If you want to buy something that isn’t a necessity, wait 48 hours. Often, the dopamine hit associated with the desire for that item will dissipate, and you will realize you don’t actually need it. By removing saved credit card information from your browser and smartphone, you add another layer of effort to the transaction, giving your brain the time it needs to shift from an emotional state back to a logical one.

Consistency: The Engine of Compound Growth

The power of compound interest is often called the eighth wonder of the world. However, it only works if you keep the engine running. People who wait until they have “enough” money to start investing often miss the most critical window for wealth building: time. Investing small, consistent amounts every single month—regardless of market volatility—is a far more effective strategy than trying to time the market with a large lump sum.

Consistency creates a safety net. It builds the resilience necessary to weather economic downturns. When you view investing as a habit rather than a gamble, you detach your emotions from the market’s performance, which is exactly how millionaires are made.

Battling Lifestyle Inflation

Every time you receive a pay raise, a dangerous psychological trap awaits: the urge to increase your standard of living to match your new income. This is known as lifestyle inflation. While it is natural to want to enjoy the fruits of your labor, letting your expenses rise in lockstep with your salary ensures you remain stuck in the paycheck-to-paycheck cycle, regardless of how much you earn.

Instead of upgrading your lifestyle, upgrade your investment rate. If you get a 5% raise, commit 3% of that to your retirement or investment account immediately. This way, your savings grow alongside your income, and you build wealth without feeling like you are restricting your current lifestyle.

The Burden of High-Interest Debt

High-interest debt is the antithesis of wealth building. It is a reverse-compound interest trap. When you carry credit card balances at 20% interest, your money is working for the lender, not for you. Prioritizing the elimination of this debt is the highest-return investment you can make.

Use the “Snowball” or “Avalanche” method to regain control. By attacking the highest interest rates first, you save thousands in interest payments over time. Once that debt is cleared, that monthly payment amount becomes your new surplus for investing. Effectively managing debt is not just about the numbers; it is about reclaiming your mental bandwidth and financial independence.

Systematizing Your Financial Life

Relying on willpower is a losing battle. Eventually, you will be tired, stressed, or tempted. A robust financial system relies on automation, not motivation. Set up your bills to autopay, your savings to auto-transfer, and your investments to auto-contribute. When these processes run in the background, you are effectively “paying yourself first” every single time you are paid.

Dedicate one Sunday each month to a “money date.” Review your progress, update your net worth spreadsheet, and ensure your spending is still aligned with your values. This small habit provides the feedback loop necessary to stay on course.

Conclusion: Wealth as a Series of Choices

Financial freedom is rarely the result of a single, monumental event. It is a quiet, deliberate accumulation of small wins. Every time you choose to brew your own coffee, every time you choose to pay off a debt rather than buy a new gadget, and every time you consistently contribute to your future, you are building wealth.

Focus on your systems, stay consistent, and avoid the trap of comparing your Chapter 1 to someone else’s Chapter 20. If you master the basics today, the compounding effect of these simple habits will guarantee your financial success in the long run. Start small, stay consistent, and watch your financial future unfold.

Frequently Asked Questions

1. Why are money habits more important than income?

Income is what you bring in, but your habits determine how much of that stays in your pocket. High earners can still be broke if their spending habits exceed their income, while average earners can build significant wealth through discipline.

2. How do I start building financial discipline?

Start with a small, manageable goal—like tracking every expense for 30 days. This creates the awareness needed to identify where you can cut back without feeling deprived.

3. Can I still build wealth if I have student loans or credit card debt?

Absolutely. The key is to create a budget that prioritizes debt repayment while still setting aside a small amount for long-term investments. This helps you build the habit of investing even while paying down liabilities.

4. How much should I be saving every month?

A common guideline is the 50/30/20 rule: 50% of income for needs, 30% for wants, and 20% for savings and debt repayment. If you can’t hit 20% yet, start with 5% or 10% and increase it incrementally.

5. Is tracking expenses time-consuming?

It can be initially, but once you set up a system (using an app or a simple spreadsheet), it takes only a few minutes each week. The insights gained are well worth the time investment.

6. What should I do if I keep failing at my budget?

Don’t aim for perfection. If you overspend one month, analyze why it happened, adjust your budget, and start fresh the next month. Consistency beats perfection every single time.

7. When is the best time to start investing?

The best time was yesterday; the second-best time is today. Compounding requires time, so starting with even small amounts as early as possible is more effective than waiting to invest large amounts later.

8. What is the most common reason people fail to build wealth?

Lifestyle inflation. As people earn more, they tend to spend more. By failing to keep expenses stable while income rises, they lose the opportunity to invest the surplus.

9. Are credit cards inherently bad for wealth building?

No, credit cards are tools. If used for convenience and paid off in full every single month, they can earn rewards and build credit scores. They only become a problem when used to spend money you don’t have.

10. Does wealth building require a special education?

Not at all. The principles of wealth building are simple: spend less than you earn, invest the difference, and stay consistent. Financial literacy is accessible to anyone willing to learn the basics.